Full Report

The numbers behind Maximus, Inc.: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings, opened with the share-price history those statements have to justify. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in US$ thousands unless noted.

Reading notes: All figures are in thousands of US dollars exactly as printed in the 10-K statements (units line: 'in thousands, except per share amounts'), except per-share and backlog rows. Each fiscal year FY2021-FY2025 is cited to its own Form 10-K (Consolidated Statements of Operations / Balance Sheets / Cash Flows and the Note 3 Business Segments table). FY2022 revenue and segment-profit cells are cited to the FY2023 10-K's comparative column (Note 3 table on p.81). Long-term record: FY2019 and FY2020 are cited to comparative columns of the FY2021 Form 10-K; FY2016-FY2018 are from the standardized data feed (SEC XBRL) and shown without page links (no filing in the corpus). Segment operating income: FY2025 is the single 'Segment operating income' line printed in the new ASU 2023-07 segment table (p.84). FY2021-FY2024 use the per-segment 'Operating income/(loss)' rows; the total segment operating income for those years is the sum of the three segments (components cited, total computed).

Share Price — Full Available History — 29 Years

The stock closed at $58.30 on Jul 17, 2026 — up 5,082% over the window shown (+14.5% a year), trading between $1.08 and $98.93. At that close the stock trades at 11× FY2025 diluted EPS as reported below.

Source: market price feed, monthly closes, sampled from 7,318 source observations, Jun 1997–Jul 2026. Price return only, excludes dividends. Prices are split-adjusted (1:2 on Jul 01, 2011; 1:2 on Jul 01, 2013).

FY2025 at a Glance

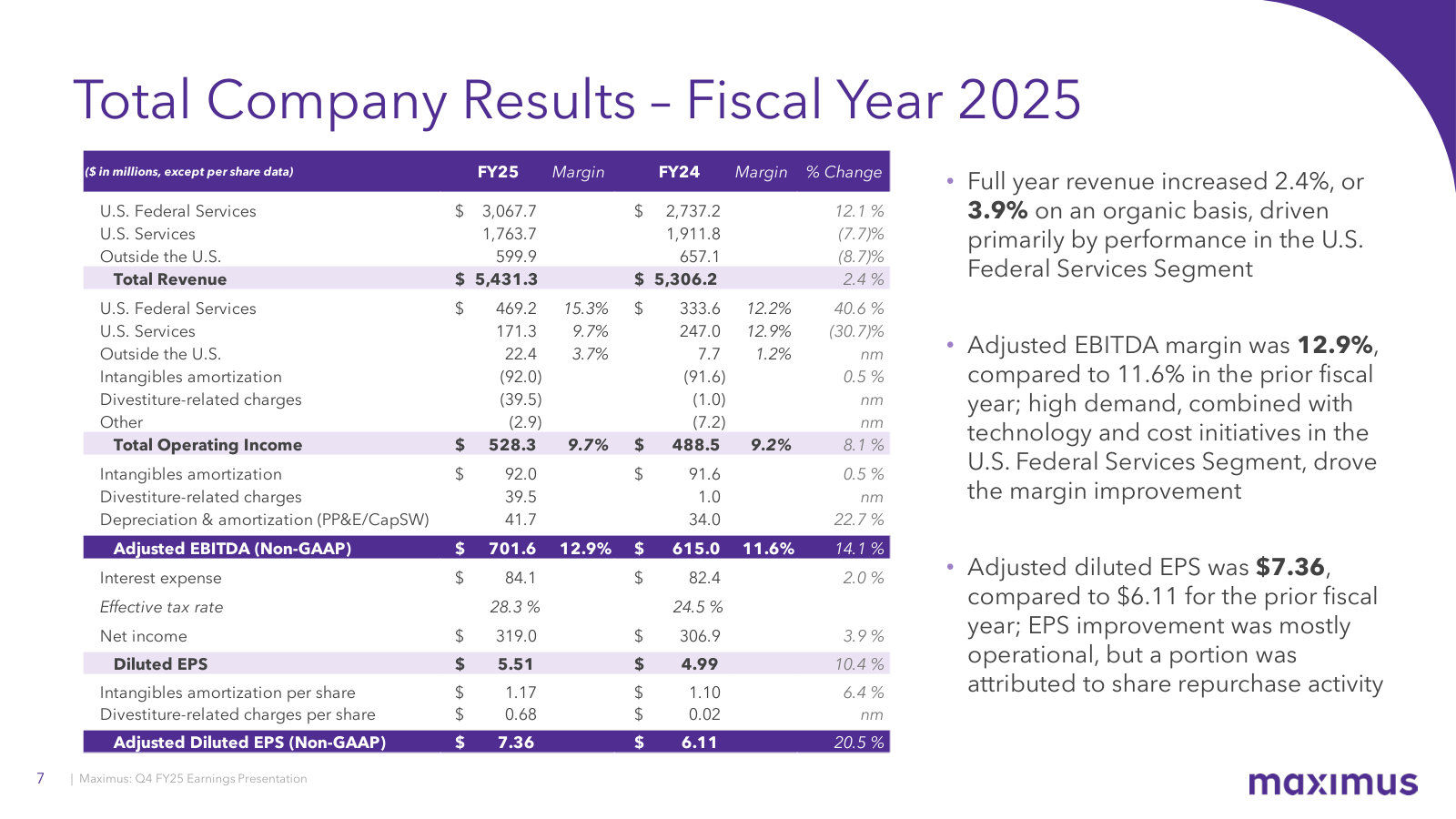

Revenue (US$ thousands)

Operating income (US$ thousands)

Net income (US$ thousands)

Diluted EPS

Source: FY2025 consolidated statements [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

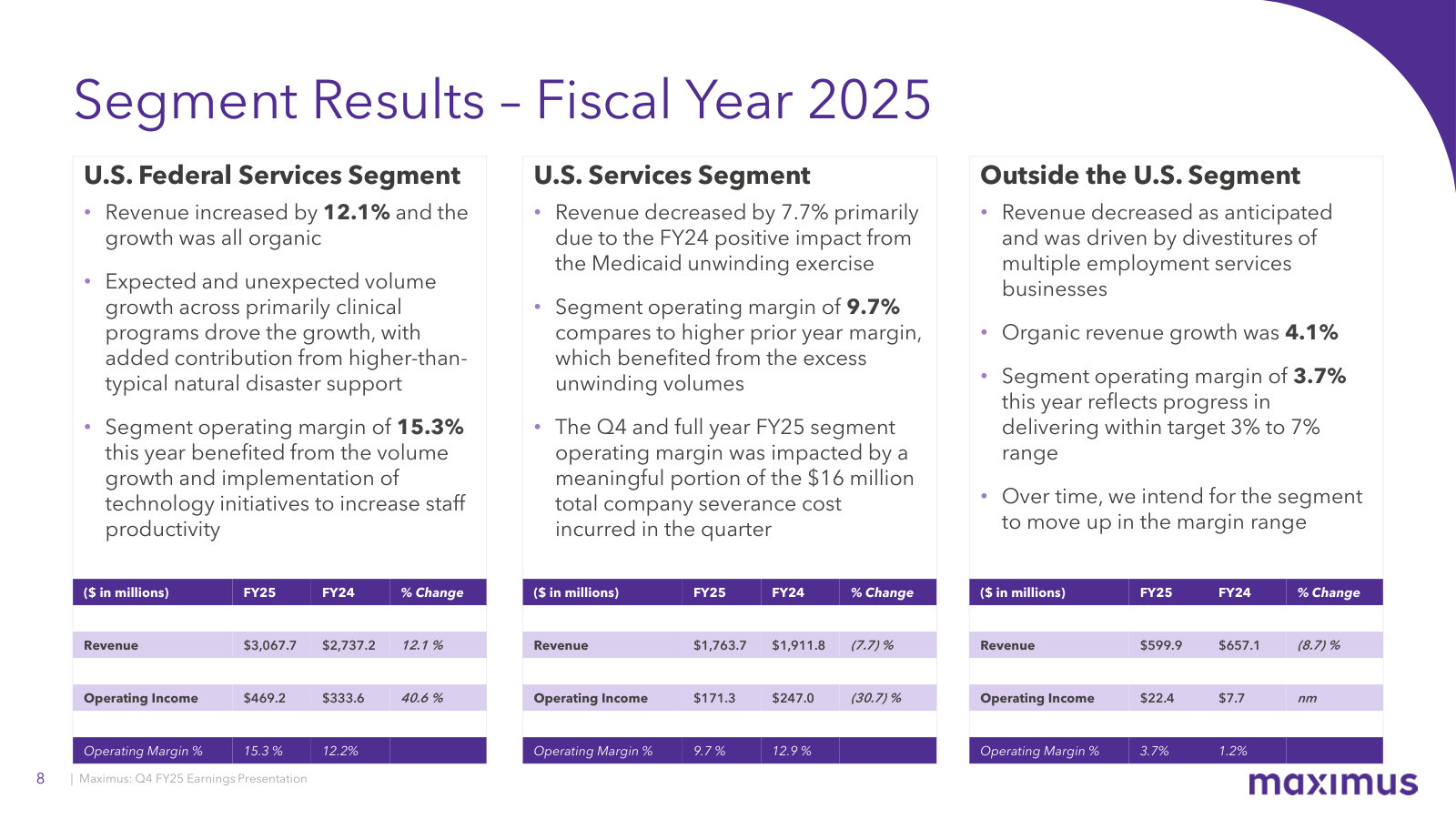

Revenue by Business Segment

| Revenue by Business Segment | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| U.S. Federal Services | 1,893,284 | 2,259,744 | 2,403,606 | 2,737,244 | 3,067,691 |

| U.S. Services | 1,662,110 | 1,607,612 | 1,812,069 | 1,911,813 | 1,763,691 |

| Outside the U.S. | 699,091 | 763,662 | 689,053 | 657,140 | 599,894 |

| Total revenue | 4,254,485 | 4,631,018 | 4,904,728 | 5,306,197 | 5,431,276 |

| Total revenue growth, derived | — | +8.9% | +5.9% | +8.2% | +2.4% |

Source: Note 3. Business Segments — Results of Operation by Business Segment (Table 3.1) [5] [6] [7] [8]. Click any linked figure to open the filing page with the row highlighted.

Segment Operating Income

| Segment Operating Income | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| U.S. Federal Services | 189,066 | 234,931 | 249,689 | 333,622 | 469,155 |

| U.S. Services | 254,441 | 182,102 | 182,550 | 246,982 | 171,264 |

| Outside the U.S. | 20,126 | (15,170) | (9,130) | 7,705 | 22,391 |

| Total segment operating income | 463,633 | 401,863 | 423,109 | 588,309 | 662,810 |

Source: Note 3. Business Segments — Results of Operation by Business Segment (Table 3.1) [5] [6] [7]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Operations [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-19. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

Source: Consolidated Balance Sheets [9] [10] [11] [12]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

Source: Consolidated Statements of Cash Flows [13] [14] [15] [16]. Click any linked figure to open the filing page with the row highlighted.

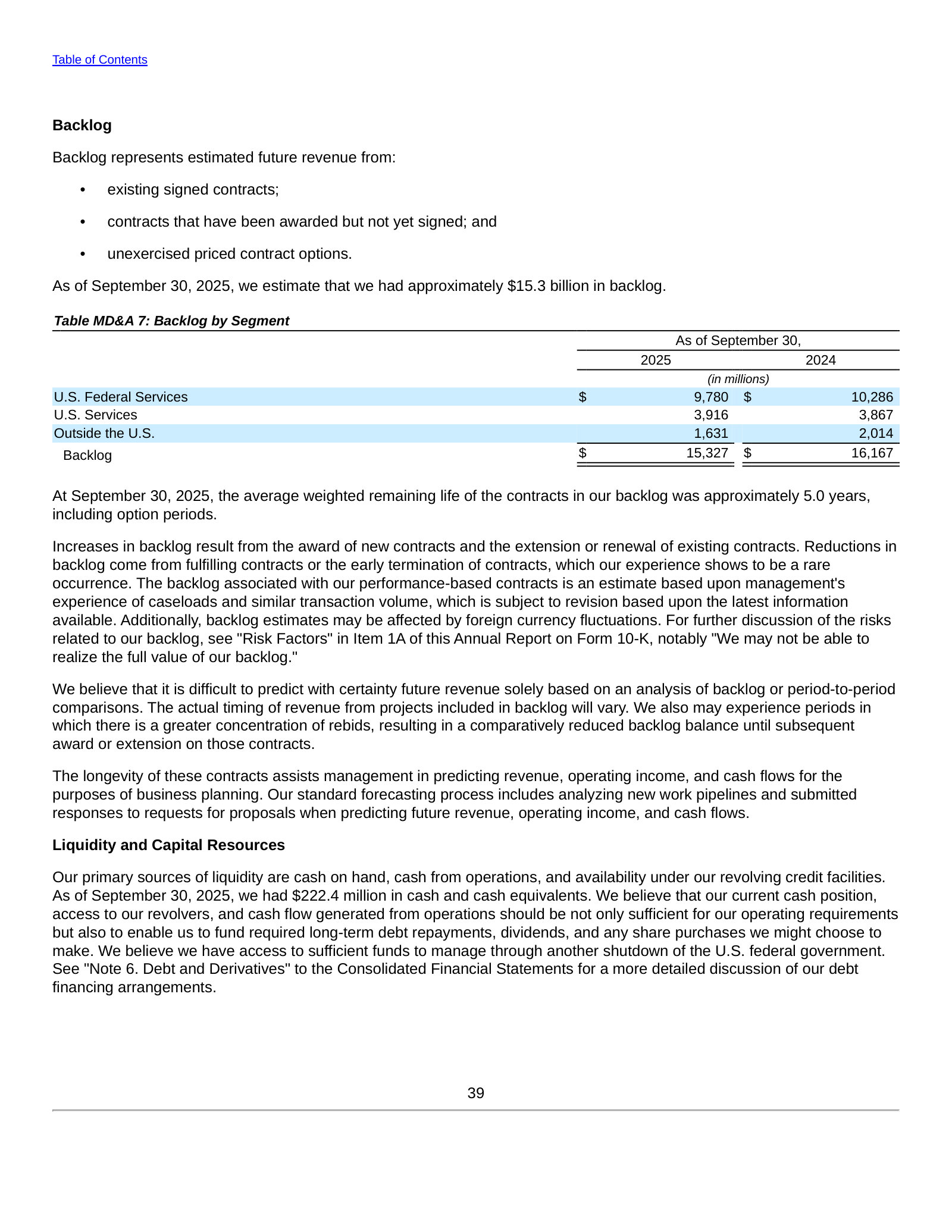

Signed Contract Backlog

| Signed Contract Backlog | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| U.S. Federal Services backlog | 4,298,000 | 13,168,000 | 13,800,000 | 10,286,000 | 9,780,000 |

| U.S. Services backlog | 4,865,000 | 5,205,000 | 4,851,000 | 3,867,000 | 3,916,000 |

| Outside the U.S. backlog | 2,052,000 | 1,441,000 | 2,089,000 | 2,014,000 | 1,631,000 |

| Total backlog | 11,215,000 | 19,814,000 | 20,740,000 | 16,167,000 | 15,327,000 |

| Weighted-avg remaining contract life (years) | 4.4 | 6.8 | 5.9 | 6.3 | 5.0 |

Source: company filings [17] [18] [19] [20]. Click any linked figure to open the filing page with the row highlighted.

Non-GAAP Profitability Cash Generation

| Non-GAAP Profitability Cash Generation | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Adjusted EBITDA | — | — | 447,861 | 615,044 | 701,554 |

| Adjusted EBITDA margin | — | — | 9.1% | 11.6% | 12.9% |

| Adjusted net income | 323,952 | 270,614 | 235,257 | 375,413 | 426,422 |

| Adjusted diluted EPS | 5.19 | 4.37 | 3.83 | 6.11 | 7.36 |

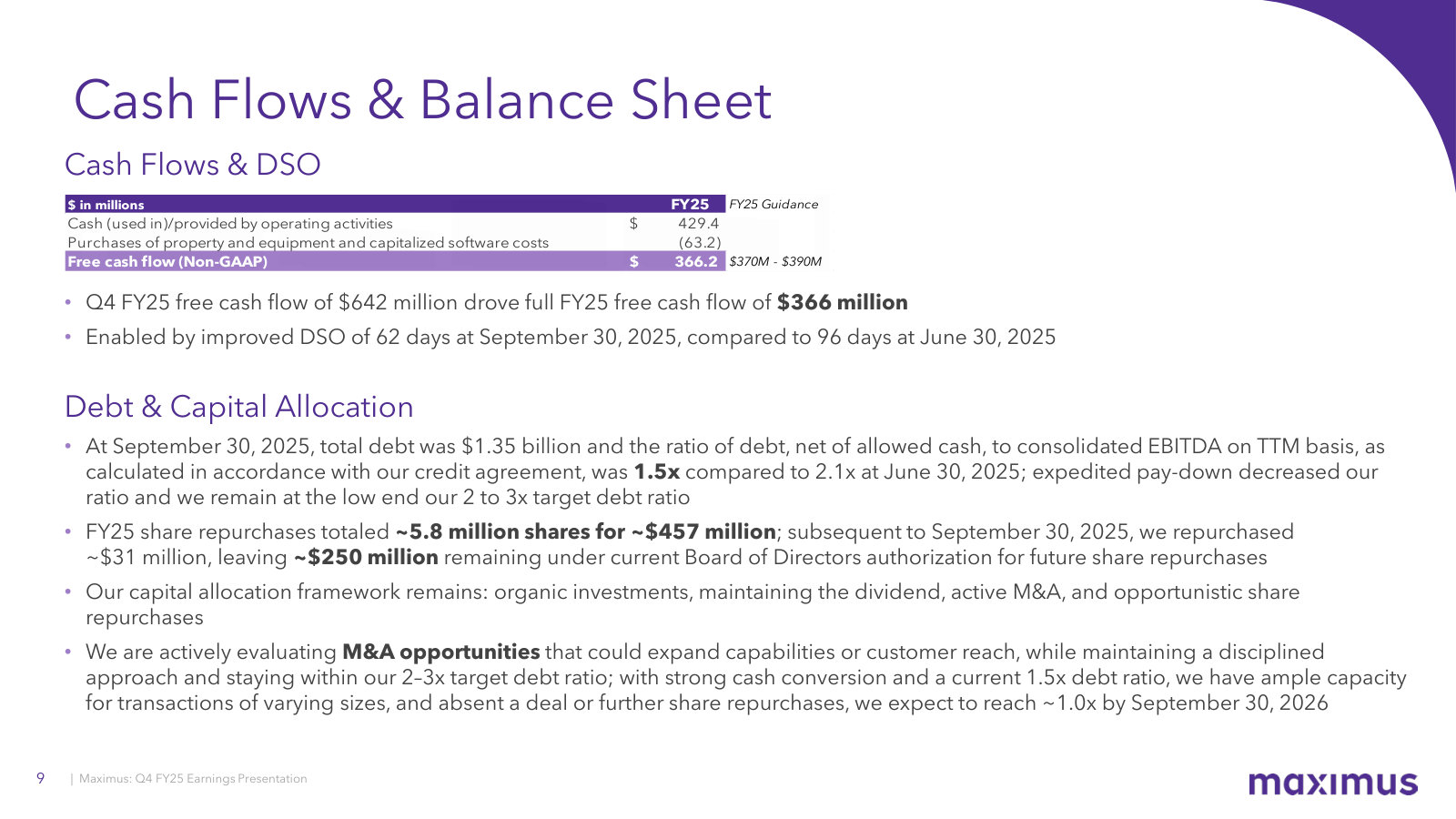

| Free cash flow (Non-GAAP) | 480,757 | 233,694 | 223,645 | 401,068 | 366,159 |

Source: company filings [21] [22] [23] [24]. Click any linked figure to open the filing page with the row highlighted.

Contract Mix Workforce

| Contract Mix Workforce | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Performance-based contracts (% of revenue) | 33.0% | 45.0% | 49.0% | 55.0% | 54.0% |

| Fixed-price contracts (% of revenue) | 13.0% | 14.0% | 15.0% | 13.0% | 13.0% |

| Days sales outstanding (days) | 68 | 62 | 60 | 61 | 62 |

| Employees | 35,800 | 39,500 | 39,600 | 41,100 | 37,200 |

| Contingent workers | 14,000 | 12,550 | 12,400 | 11,800 | 9,300 |

Source: company filings [25] [26] [27] [28]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenue | Operating income | Net income | Diluted EPS | Operating cash flow |

|---|---|---|---|---|---|

| FY2016 | — | 286,603 | 178,362 | 2.69 | 180,026 |

| FY2017 | 2,450,961 | 313,512 | 209,426 | 3.17 | 336,424 |

| FY2018 | 2,392,236 | 295,483 | 220,751 | 3.35 | 316,774 |

| FY2019 | 2,886,815 | 317,107 | 240,824 | 3.72 | 356,727 |

| FY2020 | 3,461,537 | 288,278 | 214,509 | 3.39 | 244,592 |

| FY2021 | 4,254,485 | 408,530 | 291,200 | 4.67 | 517,322 |

| FY2022 | 4,631,018 | 325,898 | 203,828 | 3.29 | 289,839 |

| FY2023 | 4,904,728 | 294,794 | 161,792 | 2.63 | 314,340 |

| FY2024 | 5,306,197 | 488,499 | 306,914 | 4.99 | 515,258 |

| FY2025 | 5,431,276 | 528,289 | 319,034 | 5.51 | 429,372 |

Source: consolidated statements across filings; older years from the standardized feed [13] [1] [14] [2]. Click any linked figure to open the filing page with the row highlighted.

Operating KPIs

| KPI | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Total backlog | 11,200,000 | 19,800,000 | 20,700,000 | 16,200,000 | 15,300,000 |

Source: company-reported operating metrics [17] [18] [19] [20]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-19. Estimate figures link to the consensus source, not to filing pages.

Traceability

363 of 381 figures on this page (95%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

All figures are in thousands of US dollars exactly as printed in the 10-K statements (units line: 'in thousands, except per share amounts'), except per-share and backlog rows.

Each fiscal year FY2021-FY2025 is cited to its own Form 10-K (Consolidated Statements of Operations / Balance Sheets / Cash Flows and the Note 3 Business Segments table). FY2022 revenue and segment-profit cells are cited to the FY2023 10-K's comparative column (Note 3 table on p.81).

Long-term record: FY2019 and FY2020 are cited to comparative columns of the FY2021 Form 10-K; FY2016-FY2018 are from the standardized data feed (SEC XBRL) and shown without page links (no filing in the corpus).

Segment operating income: FY2025 is the single 'Segment operating income' line printed in the new ASU 2023-07 segment table (p.84). FY2021-FY2024 use the per-segment 'Operating income/(loss)' rows; the total segment operating income for those years is the sum of the three segments (components cited, total computed).

Income-statement presentation: 'Other (income)/expense, net' is omitted for brevity; in the FY2021 10-K interest expense is printed as a deduction '(14,744)' whereas FY2022+ print it as a positive expense — values are stored as positive magnitudes and the anchor is the printed form.

Cash-flow outflows (capex, dividends, buybacks, acquisitions) are stored as negative values matching the printed parenthesized figures; net financing was a cash inflow in FY2021 (debt-funded VES/Aidvantage acquisitions).

Total backlog is management's approximate estimate of future revenue from the existing contract portfolio at each September 30 fiscal year end.

1 figure(s) differed between the data feed and the filing; the filing value is shown (see the run's metrics/metrics_tab.json for the audit trail).

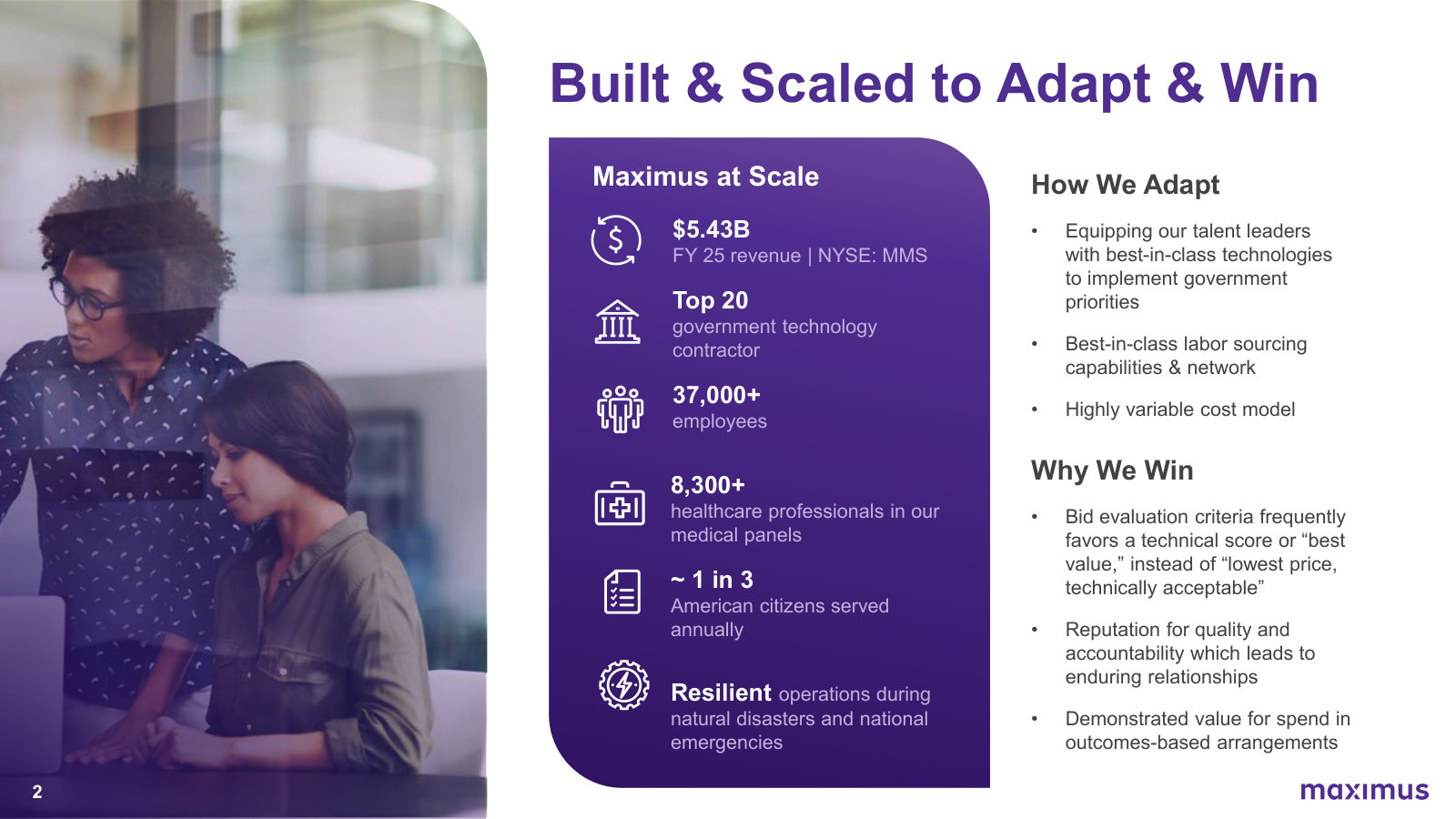

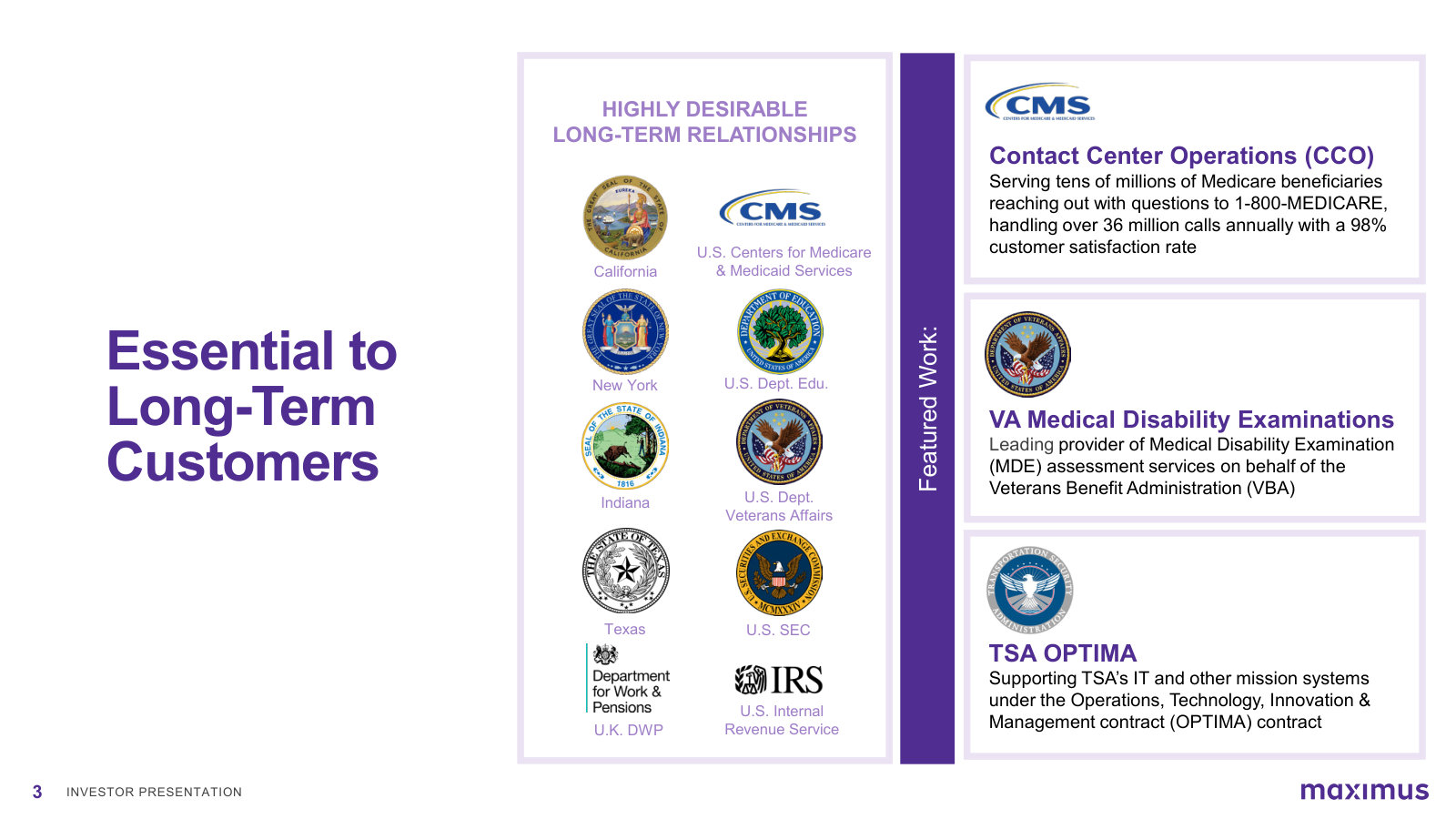

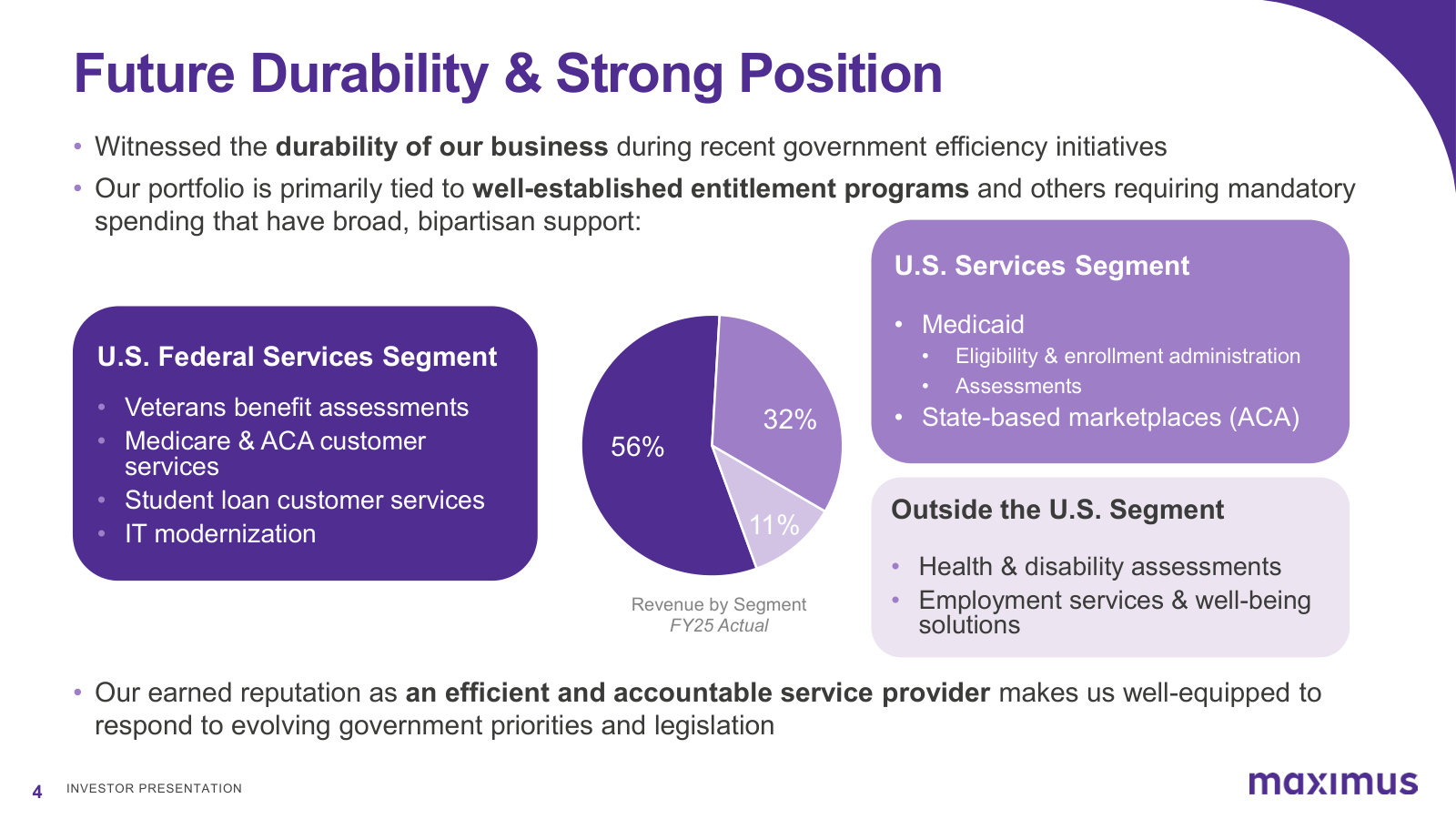

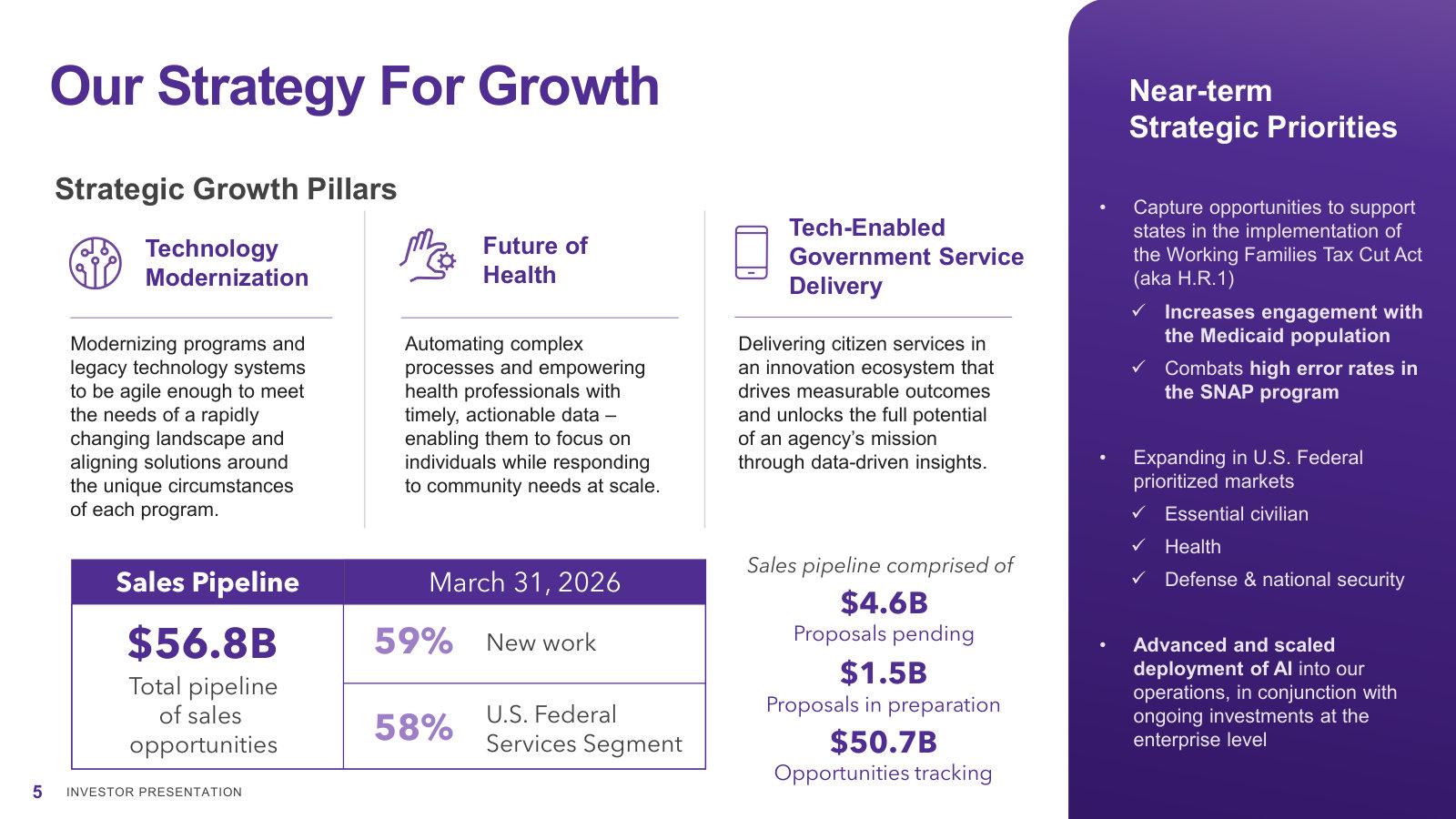

Maximus, Inc.'s management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

Investor Presentation — June 2026

Management's fullest current overview of the business — what it does, who it serves, how it gets paid, and its economic model — in one deck. · Open the full document →

Fiscal 2025 Year End Earnings Call — FY2025

The annual capstone deck: the actual segment P&L, cash flow and balance sheet behind the overview, plus FY2026 targets. · Open the full document →

More from management

Fiscal 2026 Second Quarter Earnings Call — Q2 FY2026 · 11 pages · The latest quarterly deck, with unique slides on technology-enabled program-integrity/fraud work and the maximus|TxM AI platform. · Open →

Fiscal 2024 Year End Earnings Call — FY2024 · 16 pages · The prior full-year deck — the FY2024 segment baseline the FY2025 numbers are measured against. · Open →

Fiscal 2023 Year End Earnings Call — FY2023 · 17 pages · An earlier year-end deck for the multi-year trajectory of segments, margins and cash flow. · Open →

Maximus, Inc.'s management answers for the business every quarter. These are the exchanges that explain it best — verbatim, from the call transcripts preserved in Sources. Each link opens the full transcript at that page in a new tab.

Q2 FY2026 Earnings Call — May 7, 2026

The clearest read on the current margin thesis — technology that decouples labor from volume — plus why those AI gains land in Federal and not state work, how the new H.R. 1 Medicaid/SNAP revenue is actually earned, and a candid look at elevated federal receivables. · Open the full transcript →

The core margin engine: technology embedded in programs decouples labor cost from volume, lifting Federal segment margin to 17.6%.

David Mutryn, Chief Financial Officer: The operating income margin for this segment in the second quarter was 17.6% as compared to 15.3% in the prior-year period. […] This quarter’s segment margin is delivering on that commitment thanks to technology initiatives embedded in our programs that decouple labor costs from our ability to process more volumes.

p. 2 · Read in context →

Capital-allocation discipline: buy back stock only below intrinsic value, within a 2x–3x leverage band, while still pursuing M&A.

David Mutryn, Chief Financial Officer: We have long said that we are opportunistic in our share repurchasing. To be more direct, we prioritize repurchasing when we believe our share price does not reflect the intrinsic value of the business based on a disciplined and conservative assessment. Going forward, we will continue to execute on our capital deployment priorities while considering near-term liquidity, the potential M&A opportunity set, and all within the constraint of our stated target net debt ratio of 2x to 3x. Even amidst market conditions that are favorable to share repurchases, we continue to seek acquisition targets to accelerate longer-term organic growth.

p. 2 · Read in context →

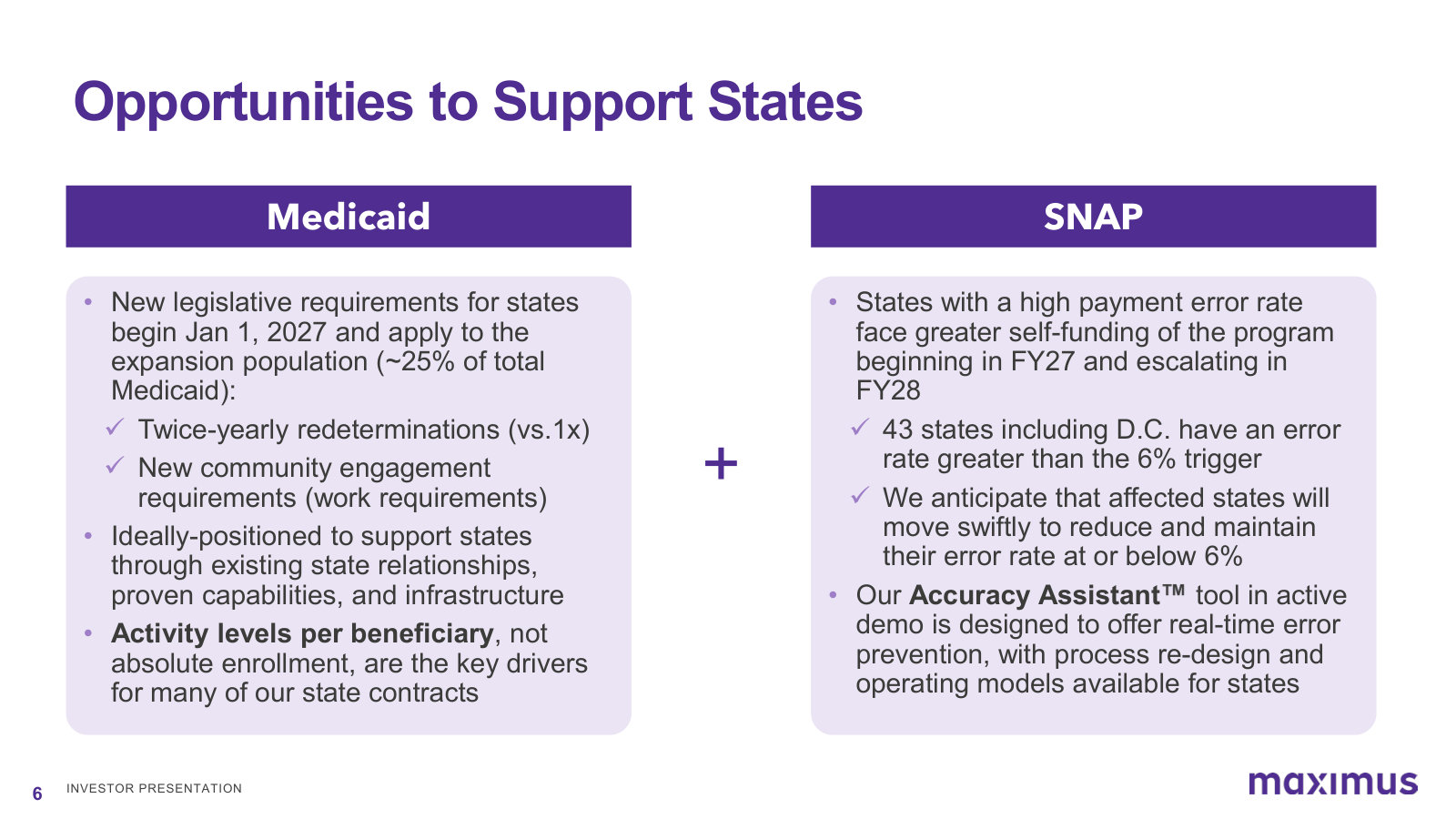

How H.R. 1 revenue is earned: a tool surfaces eligibility inconsistencies; wrapped BPO services contact beneficiaries to fix them.

Bruce Caswell, President and CEO: At the heart, it is really that tool and then the services we can wrap around it to help states identify instances where there could be inconsistencies. The tool surfaces inconsistencies in the data, and then the BPO services are used to contact beneficiaries, obtain corrections, and ensure an accurate eligibility determination. On the Medicaid side, we have a community engagement tool designed to allow beneficiaries first to navigate whether they actually need to comply with the work requirements, because they may have conditions that meet the qualifications for exemption.

p. 6 · Read in context →

The receivables scare defused: one federal program's retroactive invoicing rework on a funded contract — a timing issue, not a credit risk.

David Mutryn, Chief Financial Officer: A little more detail: this is a large program with extremely complex and data-intensive invoicing requirements. The slowdown in collections has occurred since November as we have worked with our customer on incorporating new and evolving requirements, many of which are retroactive, so may require rework of prior period invoices. This is a federal agency. We are operating under a funded contract, so we have full confidence that the outstanding invoices will be collected.

p. 6 · Read in context →

Q4 & FY2025 Earnings Call — November 20, 2025

The annual strategy call: management frames the One Big Beautiful Bill Act's Medicaid work-requirement and SNAP error-rate provisions as the biggest U.S. Services opening since the ACA, defends margin expansion on flat revenue, and points its M&A at the defense market. · Open the full transcript →

The differentiation claim: the only public peer to document its contract mix — 54.4% performance-based — betting on measurable delivery.

Bruce Caswell, President and CEO: To our knowledge, Maximus is the only public company in our sector that has formally documented its mix of contracts that are performance-based, which stands at 54.4% for fiscal year 2025. We believe this distinction reinforces our leadership in driving accountable and measurable results.

p. 2 · Read in context →

The hardest question — margins up on flat revenue: severance savings, flat SG&A despite growth, and capex rolling into amortization.

David Mutryn, Chief Financial Officer (answering CJS Securities): if you look at the margin guidance we laid out for each of the segments, all three are actually slightly higher than where they finished fiscal year 2025. […] you may notice on the P&L total company SG&A, if you consider that there was $40 million of divestiture charges in the first year in 2025, the rest of SG&A is essentially flat from 2024 to 2025 despite the revenue growth. […] a number of capitalized software projects that have been driving CapEx the past couple of years are now operational and therefore amortizing.

p. 8 · Read in context →

Where the acquisition dollars point: a defense/national-security market growing ~9%, with roughly $50B addressable to Maximus.

Bruce Caswell, President and CEO (answering CJS Securities): We've been fairly explicit with our investors in the marketplace noting that our priority in the near term is growth in the U.S. Federal market. And within that, we do have a bias toward the defense and national security space. Our research suggests that the CAGR in that area over the next several years is north of about 9%. We also believe from our research that the overall services marketplace and software spend in the defense community is well in excess of $150 billion and we believe the addressable component for Maximus to be nearly $50 billion.

p. 9 · Read in context →

Q3 FY2025 Earnings Call — August 7, 2025

The federal cost-cutting stress-test: management quantifies DOGE contract actions at under 0.5% of revenue and lays out the conflict-free, at-scale moat — enrollment broker in ~23 states, ~60% of Medicaid enrollees — that makes the coming work hard for rivals to take. · Open the full transcript →

Why a soft 0.8x book-to-bill misleads: on-contract growth (revenue +4.3%, EBITDA +15%) is its own engine when rebids are light.

Bruce Caswell, President and CEO: These awards translate into a book-to-bill of approximately 0.8x using our standard reporting for the trailing 12-month or TTM period. […] To illustrate, our book-to-bill at the end of the third quarter of fiscal year 2024 was 0.6x. Since then, revenue has grown 4.3% and adjusted EBITDA 15%, underscoring how on-contract growth is another important source of organic growth, providing added strength and resilience to our portfolio.

p. 3 · Read in context →

The moat in one answer: conflict-free, no payer or provider ties, at scale — ~23 states, ~60% of enrollees, where 'scale is everything.'

Bruce Caswell, President and CEO (answering Charles Strauzer, CJS Securities): We've said for many years that we've made a very deliberate decision to remain independent and conflict-free and in particular, have no direct or indirect financial relationships with payers or providers, which is very critical to the work that we do in the Medicaid space and to a certain degree as well with Medicare. […] But I would just say size matters in this market, and we have an established presence as the Medicaid managed care enrollment broker in about 23 states presently. We probably serve roughly 60% of the individuals nationally in the Medicaid program. As evidence in the results this quarter, scale is everything in this area of the business.

p. 8 · Read in context →

How EPS grows without revenue: deleveraging cuts interest expense $20–25M next year, worth roughly $0.30 of EPS.

David Mutryn, Chief Financial Officer (answering CJS Securities): our interest expense could be another tailwind to our EPS. If we look at our projected cash flow right just here ahead of us in the fourth quarter, as well as through next year, absent M&A or share repurchases, the deleveraging we anticipate would drive interest expense being $20 million to $25 million lower next year. So that could be like a $0.30 EPS type year-over-year improvement there.

p. 9 · Read in context →

The direct question on federal contract cuts — SEC, IRS, DOGE — met with a number: conservatively under 0.5% of FY'25 revenue.

Brian Gesuale (Raymond James); Bruce Caswell, President and CEO: Maybe you could talk about what's going on at the SEC as well as maybe anything with the IRS or any other customers that you want to discuss. […] I'm really pleased that the impact of contract actions across our portfolio has been minimal. If we had to put a number on it, conservatively less than 0.5% of our FY '25 revenues.

p. 12 · Read in context →

Q2 FY2025 Earnings Call — May 8, 2025

The first call after the DOGE shock: management puts a number on the damage (~$4M of revenue), explains why an activity-based Medicaid model can gain even as enrollment falls, and defends guidance held deliberately flat — 'downside by design.' · Open the full transcript →

The shock, quantified: DOGE actions total about $4M of FY2025 revenue — de minimis on a $5B+ base — though concession requests have begun.

Bruce Caswell, President and CEO: The impact of DOGE decisions on the business to date has been limited to a handful of small contracts where budget or scope has now been modified, some of which were already scheduled to end this fiscal year. More specifically, to date, these actions are estimated to total about $4 million in FY 2025 revenue, a de minimis figure on our base of $5 billion plus of revenue. […] As an example, like others in our sector, we have fielded requests for pricing concessions on certain contracts, which leads to a process of mutual negotiation in due course.

p. 1 · Read in context →

The counterintuitive defense: because contracts pay per activity, tighter eligibility checks can raise volumes even as rolls shrink.

Bruce Caswell, President and CEO: As discussed in February, changes that require customer engagement, such as verifying eligibility, typically increase our activity volume, which is our primary contracting model for state Medicaid programs. Therefore, a reduction in Medicaid recipients may not necessarily decrease consumer engagement, especially if eligibility verification or activity reporting requirements become more frequent than today. Additionally, in many of our largest states, we also manage state-based exchanges where customers can enroll if they are no longer eligible for Medicaid. This helps maintain our ongoing engagement with those consumers.

p. 3 · Read in context →

The candid admission: civilian-agency pipeline has slowed, but the disruption pushes work into contract bridges that favor incumbents.

Bruce Caswell, President and CEO (answering Charlie Strauzer, CJS Securities): There has been some slowdown, however, and reduction even in the pipeline in the civilian agency space. […] this has led to contract bridges and extensions that benefit incumbents, including Maximus

p. 7 · Read in context →

Q4 & FY2023 Earnings Call — November 16, 2023

The foundational teach on how Maximus makes money: the post-pandemic Medicaid 'redetermination' restart and its outsized flow-through to profit, the segment-margin mechanics behind it, and a portfolio tilting decisively toward federal work. · Open the full transcript →

The three step-ups that reshaped earnings: Medicaid redetermination restart, VA disability-exam volumes, and student-loan servicing.

David Mutryn, Chief Financial Officer: the second half of the year looked quite different from the first half as there were several sizable step-ups in earnings power of the core business as Medicaid redeterminations commenced in the third quarter in US services and volumes ramped on both the Veterans Affairs Medical Disability Exam contracts, which comprise the VES business and the student loan servicing contract in US Federal services.

p. 3 · Read in context →

The margin mechanics of the redetermination cycle: US Services swung from underweight to an 11.6% Q4 margin as paused Medicaid work resumed.

David Mutryn, Chief Financial Officer: Let me recap the margin trend of this segment. Last year, in fiscal 2022, the first half of the year was overweight from the last of the profitable short-term COVID response work, while the second half of the year was underweight. This year, the first half remained underweight until the paused Medicaid redetermination commenced in the third quarter, yielding margin improvement in the back half of the year as we expected. With the full period contribution of redeterminations US services realized an 11.6% margin in the fourth quarter.

p. 4 · Read in context →

Capital-allocation priorities, ranked: organic investment, dividend growth, then M&A — the long-term preference.

David Mutryn, Chief Financial Officer: Looking forward, our capital allocation priorities are unchanged. First, we fund organic investments, which are typically a combination of capital expenditures and expenses. Second, we maintain a dividend that we intend to grow over time with earnings and as evidenced by the recent quarterly dividend increase announcement to $0.30 per quarter. And third, strategic acquisitions intended to accelerate organic growth.

p. 5 · Read in context →

The portfolio shift: U.S. Federal went from under half of backlog two years earlier to two-thirds; a 7% dividend raise signals confidence.

Bruce Caswell, President and CEO: Just two years ago, our US Federal Services Segment accounted for less than half of our backlog. Today, the Segment makes up two-thirds of our backlog. […] During the quarter, we announced a 7% increase in our quarterly dividend, raising it to $0.30 a share. As we stated in the press release, this dividend increase demonstrates our confidence in the earnings growth reflected in our guidance.

p. 8 · Read in context →

The unit economics: redeterminations added ~$15M of quarterly US Services operating income ($40M→$55M), worth $0.15–$0.30 of EPS.

David Mutryn, Chief Financial Officer (answering Charlie Strauzer, CJS Securities): We do continue to see that contribution in line with the $0.15 to $0.30 range that we’ve given before. And I think you can see that just by looking at the total US services OI, which in Q1 and Q2 of fiscal year ’23 was more in the $40 million range per quarter. And then in Q4, it was at $55 million. So kind of a $15 million OI increase really driven by the redeterminations.

p. 14 · Read in context →

More calls

Q1 FY2026 Earnings Call — February 5, 2026 · 11 pages · The deep dive on sizing and timing the Medicaid/SNAP opportunity: management estimates a high-single to low-double-digit organic run-rate for U.S. Services by FY2028 and walks through SNAP's 6% error-rate funding trigger. · Open →

Q1 FY2025 Earnings Call — February 6, 2025 · 8 pages · Early-transition resilience: the durable, entitlement-tied portfolio that survived the federal hiring freeze and OMB grant pause, plus the secured CMS Contact Center and VA disability-exam rebids. · Open →

Q4 & FY2024 Earnings Call — November 20, 2024 · 12 pages · The annual call on the eve of the Trump transition: how a ~50-year government partner prepares for procurement delays and DOGE, why it de-risked FY2025 guidance to ~2% new work, and the switch to reporting adjusted EBITDA. · Open →

Q3 FY2024 Earnings Call — August 7, 2024 · 10 pages · The contested $6.6B CMS Contact Center recompete and GAO protest, cost-plus contract economics, election-outcome resilience, and how FY2024's excess redetermination volumes normalize into FY2025. · Open →

Q2 FY2024 Earnings Call — May 8, 2024 · 9 pages · The Medicaid 'unwind' ends and reverts to business-as-usual, both domestic segments hit the top of their margin targets, and management weighs whether to even bid the labor-harmony CCO recompete. · Open →

Q1 FY2024 Earnings Call — February 7, 2024 · 10 pages · Why volumes swing profit disproportionately — 53% of revenue is performance-based — with the redetermination margin at a 13.5% high-water mark and the cost-plus CCO contract's economics disclosed. · Open →

Q3 FY2023 Earnings Call — August 3, 2023 · 8 pages · The mechanics of the Medicaid redetermination ramp: why volumes built slowly (ex parte renewals, hard-to-reach cohorts), plus the student-loan repayment restart and a MOVEit cyber charge. · Open →

Q4 & FY2021 Earnings Call — November 18, 2021 · 26 pages · The COVID-era playbook: standing up ~13,000 agents fast on a variable-cost model, four acquisitions including the Aidvantage student-loan servicing entry, and a back-loaded FY2022 built on the UK Restart program. · Open →

Maximus, Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

Maximus, Inc. — FY2025 Annual Report (Form 10-K) — FY2025

Latest 10-K; the fullest account of how a government-services contractor earns, where its revenue concentrates, and the policy/budget risks that could bite. · Open the full document →

Item 1. Business — General — p. 8 · Read the full section →

The core self-definition: a tech-enabled services provider that turns public policy into operating models delivered at scale.

What Maximus is and how it says it creates value.

Maximus, a Virginia corporation established in 1975 and celebrating its 50th anniversary this year, is a leading provider of tech-enabled services to government agencies. […] We create value for our customers through our ability to translate public policy into operating models that achieve outcomes for governments at scale.

p. 8 · Read in context →

Item 1. Business — Our Business Segments — p. 9 · Read the full section →

Defines the three operating segments and the revenue concentration — U.S. Federal Services alone is 56% of the top line.

Three segments; U.S. Federal Services is the majority of revenue.

We operate our business through three segments: U.S. Federal Services, U.S. Services, and Outside the U.S. We operate in the United States and worldwide. […] Our U.S. Federal Services Segment generated 56% of our total revenue in fiscal year 2025.

p. 9 · Read in context →

Item 1A. Risk Factors — p. 22 · Read the full section →

The two risks specific to this business model: dependence on government appropriations/shutdowns, and cyber breaches of the citizen data it holds.

Custodian of citizen and health data — a breach threatens contracts, sanctions and client confidence.

The risk of a security breach, system disruption, ransom-ware attack, or similar cyber-attack or intrusion, including by computer hackers, cyber terrorists, or foreign governments, is persistent, substantial, and increases as the volume, intensity, and sophistication of attempted attacks, intrusions and threats from around the world increase daily. […] The loss, theft, or improper disclosure of that information could subject us to sanctions under the relevant laws, breach of contract claims, contract termination, class action, or individual lawsuits from affected parties, negative press articles, reputational damage, and a loss of confidence from our government clients, all of which could adversely affect our existing business, future opportunities, and financial condition.

p. 29 · Read in context →

Item 1C. Cybersecurity — p. 41 · Read the full section →

Discloses the FY2023 MOVEit incident as a material event — the concrete instance of the breach risk, with governance detail.

The material FY2023 incident: a zero-day in a third-party file-transfer vendor exposed personal data.

We have experienced cybersecurity incidents that were immaterial and, as previously disclosed, in the third quarter of fisca year 2023, we experienced a material cybersecurity incident as the personal information of a significant number of individuals was accessed by an unauthorized third-party exploiting a zero-day vulnerability in a third-party vendor's file transfer application used by many organizations, including us.

p. 41 · Read in context →

Item 7. MD&A — Results of Operations — p. 49 · Read the full section →

The consolidated P&L plus a revenue bridge that separates organic growth from the Outside-U.S. divestitures and FX.

Item 7. MD&A — U.S. Federal Services Segment — p. 51 · Read the full section →

Management's own account of what drove the year: clinical/medical assessments, the PACT Act, and FEMA disaster support lifting margin to 15.3%.

The growth drivers: clinical programs, FEMA support and PACT Act–driven assessment volumes.

Our revenue growth was driven by our clinical programs, including medical assessments, as well as from support provided to the Federal Emergency Management Agency (FEMA). […] Our medical assessment revenue benefitted from increased volumes, including those driven by the Honoring our Pact Act, which had necessitated a contract rebid to expand the scale of these arrangements, as well as volume increases from underlying assessment demands.

p. 51 · Read in context →

Item 7. MD&A — Backlog — p. 54 · Read the full section →

Revenue visibility for a contractor: $15.3bn of backlog with a ~5.0-year weighted remaining life, split by segment.

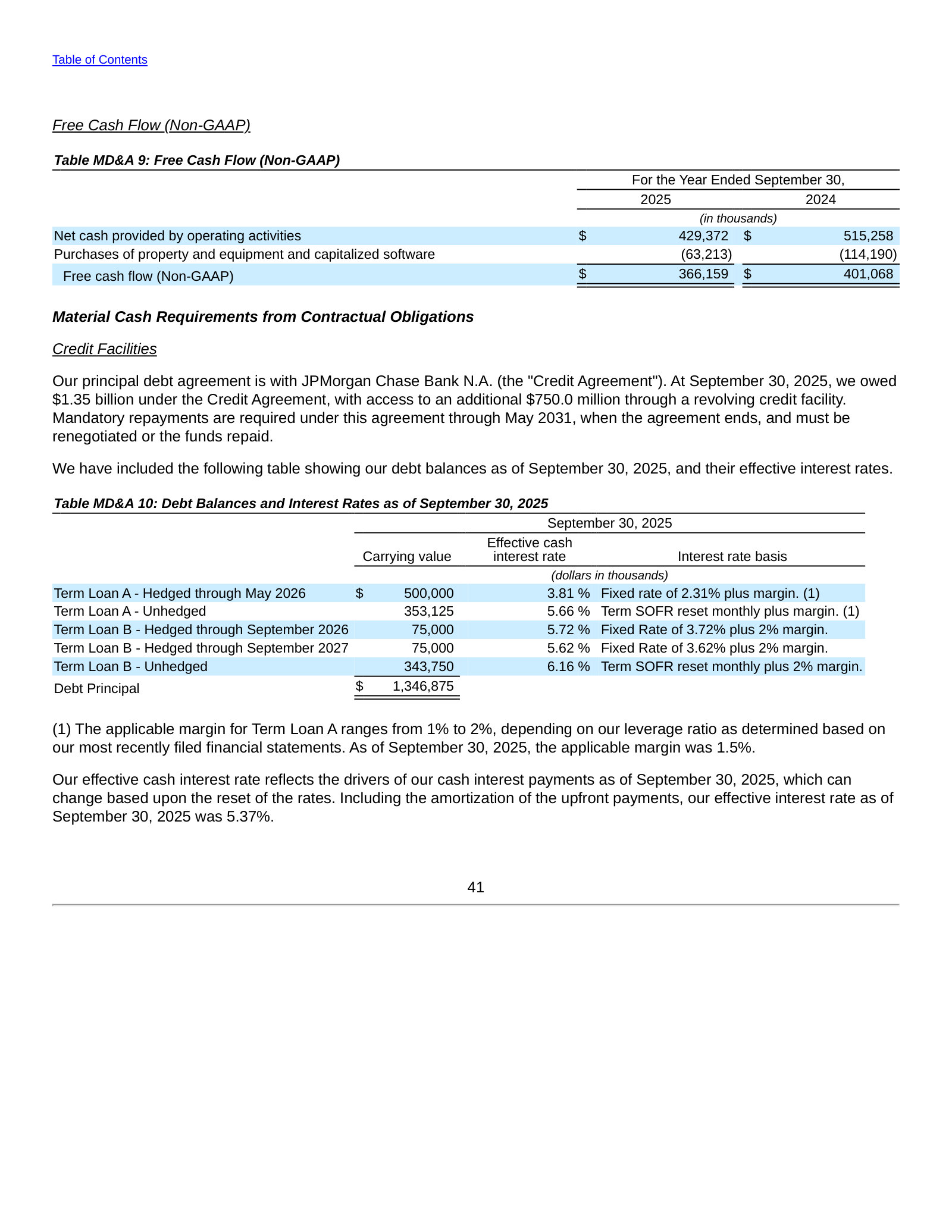

Item 7. MD&A — Free Cash Flow and Credit Facilities — p. 56 · Read the full section →

The non-GAAP free-cash-flow reconciliation and the $1.35bn term-loan schedule that debt reduction is prioritized against.

Critical Accounting Policies — Revenue Recognition — p. 59 · Read the full section →

The policy that defines the model: performance-based contracts carry variable consideration estimated by expected value and constrained against reversal.

Penalties and incentives are variable consideration, estimated and constrained each period.

Certain performance-based contracts include variable consideration in the form of penalties and incentives, based on our performance under the terms of the contract. The calculation of these penalties and incentives requires the evaluation of both objective and subjective criteria, which may require the use of estimates. […] We estimate the total variable consideration we will receive using the expected value method. […] We are required to constrain our estimates to the extent that it is probable that there will not be a significant reversal of cumulative revenue when the uncertainty is resolved.

p. 59 · Read in context →

More annual reports

Maximus, Inc. — FY2024 Annual Report (Form 10-K) — FY2024 · 117 pages · The prior year's baseline for the FY2025 comparisons — revenue $5.31bn and the segment mix before further Outside-U.S. divestitures. · Open →

Maximus, Inc. — FY2023 Annual Report (Form 10-K) — FY2023 · 114 pages · First disclosure of the MOVEit cybersecurity incident and the start of the Outside-U.S. reshaping/divestiture program. · Open →

Maximus, Inc. — FY2022 Annual Report (Form 10-K) — FY2022 · 119 pages · The pre-divestiture Outside-U.S. footprint and peak pandemic-response work, useful as an evolution reference. · Open →

Maximus, Inc. — FY2021 Annual Report (Form 10-K) — FY2021 · 124 pages · The earliest edition on the shelf — segment structure and disclosures before the recent strategy reset. · Open →

Competitors describe Maximus, Inc.'s market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

Conduent (CNDT)

The closest US-listed pure-play government-services BPO rival to Maximus: its Government segment administers Medicaid healthcare, eligibility and enrollment, benefits payments and case management for federal, state and local agencies — the same programs that anchor Maximus's US Services and US Federal Services segments.

Conduent's own sizing of the business-process-services market it and Maximus compete in — an addressable $219 billion in 2025 where it claims analyst-recognized leadership.

We estimate our addressable market size in the global business process services industry to be $219 billion in 2025, according to third-party industry reports. Many industry analysts and advisors place us as a leader across several segments in this large, diverse and growing market.

p. 7 · Read in context →

Conduent's description of its government portfolio reads as a point-for-point overlap with Maximus's core work — Medicaid claims, eligibility determination, enrollment and benefits delivery for state agencies.

Our government portfolio includes government healthcare, eligibility and enrollment solutions, digital payments and child support payments, ensuring efficient Medicaid healthcare claims processing and delivery of benefits to the most vulnerable populations while reducing the risk of fraud. Our solutions help state agencies determine eligibility, streamline enrollment, adjudicate claims and meet requirements for government-funded healthcare programs.

p. 5 · Read in context →

On its Q1 FY2026 call, Conduent quantifies a re-entry into the federal health-and-human-services market — Maximus's home turf — led by a $23 million government-Medicaid-claims win.

Cliff Skelton, President & CEO: In the Public Sector segment, we signed more than $66 million in new business in Q1. This was driven by a large deal in government Medicaid claims for $23 million in new business.

p. 2 · Read in context →

Serco Group (SRP.L)

A global government-services outsourcer that competes head-on with Maximus in US and UK citizen services — most directly through Serco Inc.'s CMS Eligibility Support Services contract running eligibility and contact-center support for the health-insurance Exchanges, the franchise at the heart of Maximus.

Serco's FY2025 report details its CMS Eligibility Support Services contract — eligibility and enrollment support for the ACA health-insurance Exchanges, the same CMS work that is Maximus's flagship US contract.

CMS Eligibility Support Services contract: In July 2023, Serco Inc. was awarded a follow-on contract with the US Government (acting through the Centers for Medicare and Medicaid Services (CMS)) for the provision of support for the Exchanges implemented to provide affordable health insurance and insurance affordability programmes.

p. 131 · Read in context →

Serco management sizes its US government-services business and frames the runway — a $2 billion portfolio it estimates is still only just over 1% of the market Maximus also serves.

Anthony Kirby, CEO: In recent years, we've doubled the revenue and tripled the profit of our U.S. business to a $2 billion portfolio, delivering 10% margins, and we estimate that we still only have just over 1% market share.

p. 10 · Read in context →

Serco reports a decade-high bid pipeline, a measure of the competitive capacity chasing the same government contracts Maximus bids for.

Our pipeline was £12.1bn at the end of December 2025, 8% higher than the £11.2bn level at the end of December 2024 and the highest level in over a decade. The pipeline consists of over 70 bids, with an average ACV of £30m and an average contract length of around five years.

p. 25 · Read in context →

Capita (CPI.L)

The UK government's self-described number-one BPS supplier and the one competitor that names Maximus directly; its Public Service division runs the Health Assessment Advisory Service and other citizen-services contracts that collide with Maximus's UK health-and-disability-assessment and welfare-to-work businesses.

Capita's Public Service division lists its competitors in the UK government market and names Maximus explicitly — the one direct competitor filing in this set to do so.

Public Service operates in highly fragmented markets with a variety of services offered. Competitors within the market include but are not limited to: Atos, G4S, Sopra Steria, CGI, Tata Consulting Services, Serco, Accenture and Maximus.

p. 8 · Read in context →

Capita attributes Public Service growth to the Health Assessment Advisory Service and disability-related contract wins — precisely the UK clinical-assessment and welfare lines Maximus operates.

strong performance in Public Service which saw growth from the Health Assessment Advisory Service and Disabled Student Allowance contract wins and growth from existing contracts including Transport for London and the Royal Navy training contract.

p. 7 · Read in context →

Capita quantifies its UK government contract-win momentum — £1.19bn of total contract value, up 28% — including an NHS England contract, a benchmark of competitive scale against Maximus's UK footprint.

Across 2025, Public Service won contracts with a TCV of £1,185.8m, up 28% from 2024. There were material wins with Education Authority Northern Ireland, Gas Safe Register and with NHS England on our PCSE contract and a further expansion of scope on our successful contracts with the Royal Navy.

p. 9 · Read in context →

Leidos (LDOS)

Through Leidos QTC, the largest provider of government-outsourced medical disability examinations — the clinical-assessment business Maximus also performs for the VA and, internationally, through its health-assessment contracts. Its Health & Civil segment is a direct read on that market's economics.

Leidos reports high veterans' disability-exam volume through its QTC clinics — the government medical-examination business it and Maximus both compete in.

Tom Bell, CEO: in our ongoing Veterans Benefits exam business, I'm pleased to report that our disability exam volume remained high through the first quarter and customer satisfaction, veteran satisfaction with their treatment at Leidos QTC clinics remains best in class.

p. 2 · Read in context →

Leidos ties its Health & Civil segment's ~25% margin to medical-disability-exam volume — a benchmark for the profitability of the clinical-assessment work Maximus performs.

Health and Civil revenues increased by 1% year-over-year, with a non-GAAP operating income margin of 24.9%. Sustaining high performance levels was due to a consistent high volume of medical disability exams and our team's unwavering focus on delivering excellent innovation.

p. 3 · Read in context →

Leidos management acknowledges the VA disability-exam market is a contested multi-vendor field — a fourth provider has entered — the same competitive dynamic that shapes Maximus's exam share.

Tom Bell, CEO: As you may have noticed, a fourth provider has been introduced in some regions, and we recognize that we need to stay ahead of the competition through innovation and technology, ensuring strong performance and customer satisfaction.

p. 7 · Read in context →

ICF International (ICFI)

A federal-focused consulting and digital-services firm whose largest client is HHS — overlapping Maximus's health-and-human-services and government-modernization work — and whose disclosures document the DOGE-era budget pressure that is the shared macro risk for government-services vendors.

ICF quantifies its federal-government dependence and names HHS among its most significant clients — the same federal-health demand pool Maximus relies on — with federal revenue falling to 43% in 2025.

Our largest clients are U.S. federal government departments and agencies. Our federal government clients include every cabinet-level department, most significantly HHS, DoD, DoE, and DoT. Federal government clients generated approximately 43%, 54%, and 55% of our revenue in 2025, 2024, and 2023, respectively.

p. 38 · Read in context →

ICF discloses DOGE-driven contract terminations and stop-work orders in early 2025 — concrete evidence of the federal-spending disruption that is the shared risk across Maximus's peer set.

we received contract terminations and temporary stop-work orders primarily in the first and second quarters of 2025. We expect that, due to changing government budgeting and spending priorities

p. 19 · Read in context →

SAIC (SAIC)

A large federal IT and digital-modernization contractor; while defense-weighted, its priority civilian segment serves the same civilian agencies (Treasury/IRS, State, DHS, DOT/FAA) that fund Maximus's citizen-services and modernization work, making its federal-demand read-through relevant.

SAIC's CEO sizes the FY2026 civilian-agency funding backdrop — DOT/FAA and DHS budgets — the same non-defense federal pool that funds Maximus's government-services work.

Toni Townes-Whitley, CEO: Regarding nondefense budgets, the areas of focus for Science Applications International Corporation at our five largest civilian agency customers were well supported, including over $1 billion of additional budget for the Department of Transportation to fund improvements at the FAA. Over $40 billion to the Department of Homeland Security, focused in part on procuring advanced border security technology.

p. 2 · Read in context →

SAIC management frames its separately-reported civilian business as a priority growth area — the civilian-agency digital-modernization space Maximus also targets.

Toni Townes-Whitley, CEO: So let's start with our civilian business. As you know, we report that separately. We've been focusing on really over even over the last year as we said the civilian business was a critical one for us. We want to see further growth in that business, and we have seen quite frankly growth in that business.

p. 6 · Read in context →

More peer documents

Q4_FY2025 — 9 pages · Conduent's FY2025 wrap-up, with CEO commentary sizing US Medicare/healthcare spending and the eligibility complexity created by new legislation — the demand backdrop for the health-program market. · Open →

CNDT_annual_report_FY2024 — 100 pages · Prior-year 10-K with the same Government-segment and Medicaid-services description — useful for a two-year view of Conduent's public-sector positioning against Maximus. · Open →

Q2_FY2024 — 17 pages · Serco calls its CMS health-eligibility contract a group-wide benchmark for technology-enabled productivity — the automation narrative that overlaps Maximus's ACA/Medicaid franchise. · Open →

LDOS_annual_report_FY2025 — 117 pages · Leidos 10-K Health & Civil segment detail — segment revenue scale (~$5bn) and margins that frame the government-health/medical-exam market Maximus competes in. · Open →

Q4_FY2025 — 13 pages · Leidos quantifies a ~60% cut in the VA exam backlog and flags the 2026 disability-exam recompete — the contract dynamics driving competition for exam share. · Open →

Q4_FY2025 — 13 pages · ICF reports ~$1.1bn of 2025 federal awards and a high-single-digit 2026 federal-revenue-decline outlook — a peer read on federal award momentum and the DOGE-era demand reset. · Open →

SAIC_annual_report_FY2025 — 100 pages · SAIC 10-K with total backlog of ~$22.6bn (Civilian ~$4.2bn) and the continuing-resolution funding backdrop — a scale and budget-environment benchmark for government-services vendors. · Open →

Q4_FY2024 — 19 pages · Capita's results call, with a ~£19.8bn unweighted pipeline and improved win rates — competitive-capacity detail behind its UK Public Service positioning versus Maximus. · Open →

Source: S&P Capital IQ consensus via Xpressfeed · Generated 2026-07-19.

Street snapshot

Coverage is thin at two analysts, both rating the stock outperform, for a consensus recommendation score of 2. Their price targets span USD 85 to 125 around a 105 mean and median.

Currency: USD · Scale: money in millions, absolute (per share) · Analyst counts shown explicitly; recommendation respondents: 2.

| Street view | Reading | Analysts |

|---|---|---|

| Recommendation mix | Buy 0, Outperform 2, Hold 0, Underperform 0, Sell 0 | 2 |

| Consensus score | 2.00 | 2 |

| Target price | mean 105.0; high 125.0; low 85.00 | 2 |

Forward table

Revenue is seen dipping from about USD 5,454m in FY2025 to USD 5,296m in FY2026 before recovering to USD 5,551m in FY2027, while normalized EPS still climbs from 7.45 to 9.07 and gross margin edges up from 24.4% toward 25%. EBITDA rises across the window from 707m to 784m, so the earnings path looks driven more by margin than by top-line growth.

Currency: USD · Scale: money in millions, absolute (per share) · Analyst count is the estimate count for each period and metric.

| Period | Metric | Mean | YoY | Analysts | Low / high |

|---|---|---|---|---|---|

| FY0E | Revenue | 5,296 | -2.5% | 2 | 5,274 / 5,318 |

| FY0E | EBITDA | 749.5 | 6.8% | 2 | 747.9 / 751.0 |

| FY0E | EBIT | 619.9 | 15.4% | — | — / — |

| FY0E | Net income (GAAP) | 404.4 | 26.8% | 2 | 403.3 / 405.5 |

| FY0E | Net income (normalized) | 459.9 | 6.7% | — | — / — |

| FY0E | EPS (GAAP) | 7.43 | 34.9% | 2 | 7.41 / 7.46 |

| FY0E | EPS (normalized) | 8.44 | 14.6% | 2 | 8.40 / 8.47 |

| FY0E | Gross margin | 25.4% | 4.1% | — | — / — |

| FY+1E | Revenue | 5,551 | 4.8% | 2 | 5,503 / 5,598 |

| FY+1E | EBITDA | 784.0 | 4.6% | 2 | 767.9 / 800.2 |

| FY+1E | EBIT | 653.6 | 5.4% | — | — / — |

| FY+1E | Net income (GAAP) | 427.6 | 5.7% | 2 | 424.5 / 430.7 |

| FY+1E | Net income (normalized) | 490.6 | 6.7% | — | — / — |

| FY+1E | EPS (GAAP) | 7.96 | 7.0% | 2 | 7.86 / 8.05 |

| FY+1E | EPS (normalized) | 9.07 | 7.5% | 2 | 8.95 / 9.19 |

| FY+1E | Gross margin | 25.3% | -0.4% | — | — / — |

| Q3 FY2026 | Revenue | 1,327 | -1.6% | 2 | 1,311 / 1,344 |

| Q3 FY2026 | EBITDA | 192.5 | -2.9% | 2 | 188.9 / 196.1 |

| Q3 FY2026 | EBIT | 159.9 | 36.6% | — | — / — |

| Q3 FY2026 | Net income (GAAP) | 103.7 | -2.1% | 2 | 100.7 / 106.8 |

| Q3 FY2026 | Net income (normalized) | 121.7 | 31.1% | — | — / — |

| Q3 FY2026 | EPS (GAAP) | 1.93 | 3.5% | 2 | 1.87 / 1.98 |

| Q3 FY2026 | EPS (normalized) | 2.21 | 2.1% | 2 | 2.15 / 2.26 |

| Q3 FY2026 | Gross margin | 25.7% | 11.0% | — | — / — |

| Q4 FY2026 | Revenue | 1,317 | -0.1% | 2 | 1,311 / 1,323 |

| Q4 FY2026 | EBITDA | 198.5 | 23.9% | 2 | 196.5 / 200.5 |

| Q4 FY2026 | EBIT | 165.9 | 26.1% | — | — / — |

| Q4 FY2026 | Net income (GAAP) | 109.2 | 45.0% | 2 | 107.9 / 110.5 |

| Q4 FY2026 | Net income (normalized) | 122.9 | 25.4% | — | — / — |

| Q4 FY2026 | EPS (GAAP) | 2.04 | 54.2% | 2 | 2.02 / 2.05 |

| Q4 FY2026 | EPS (normalized) | 2.31 | 42.3% | 2 | 2.28 / 2.33 |

| Q4 FY2026 | Gross margin | 26.0% | 6.1% | — | — / — |

| Q1 FY2027 | Revenue | 1,409 | 4.8% | 1 | 1,409 / 1,409 |

| Q1 FY2027 | EBITDA | 200.7 | 17.8% | 1 | 200.7 / 200.7 |

| Q1 FY2027 | EBIT | 167.4 | 21.9% | — | — / — |

| Q1 FY2027 | Net income (GAAP) | 107.6 | 14.6% | 1 | 107.6 / 107.6 |

| Q1 FY2027 | Net income (normalized) | 122.6 | 12.7% | — | — / — |

| Q1 FY2027 | EPS (GAAP) | 2.02 | 18.8% | 1 | 2.02 / 2.02 |

| Q1 FY2027 | EPS (normalized) | 2.31 | 24.9% | 1 | 2.31 / 2.31 |

| Q1 FY2027 | Gross margin | 25.1% | 9.6% | — | — / — |

| Q2 FY2027 | Revenue | 1,380 | 5.7% | 1 | 1,380 / 1,380 |

| Q2 FY2027 | EBITDA | 195.4 | 3.9% | 1 | 195.4 / 195.4 |

| Q2 FY2027 | EBIT | 163.1 | 14.1% | — | — / — |

| Q2 FY2027 | Net income (GAAP) | 104.5 | 6.6% | 1 | 104.5 / 104.5 |

| Q2 FY2027 | Net income (normalized) | 119.5 | 8.6% | — | — / — |

| Q2 FY2027 | EPS (GAAP) | 1.96 | 8.9% | 1 | 1.96 / 1.96 |

| Q2 FY2027 | EPS (normalized) | 2.24 | 8.2% | 1 | 2.24 / 2.24 |

| Q2 FY2027 | Gross margin | 25.0% | 4.6% | — | — / — |

Estimate momentum

Only FY2027 carries revision history here. Over the past 180 days normalized EPS consensus rose from 8.68 to 9.07 while revenue was trimmed from 5,741m to 5,551m, and both were essentially unchanged over the last 30 days.

Currency: USD · Scale: money in millions, absolute (per share) · Point-in-time consensus; analyst count is shown where supplied.

| Period | Metric | Lookback | Then | Now | Direction / magnitude | Analysts |

|---|---|---|---|---|---|---|

| 2027 | EPS (normalized) | 30d | 9.07 | 9.07 | flat 0.0% | — |

| 2027 | EPS (normalized) | 90d | 9.12 | 9.07 | down 0.5% | — |

| 2027 | EPS (normalized) | 180d | 8.68 | 9.07 | up 4.5% | — |

| 2027 | Revenue | 30d | 5,551 | 5,551 | flat 0.0% | — |

| 2027 | Revenue | 90d | 5,680 | 5,551 | down 2.3% | — |

| 2027 | Revenue | 180d | 5,741 | 5,551 | down 3.3% | — |

Beat / miss record

Across the last eight quarters normalized EPS has beaten consensus in six, including outsized 45.7% and 40.7% surprises in the quarters ended March and June 2025. Revenue is more mixed, swinging from mid-single-digit beats into three straight small misses in the most recent quarters.

Current sequences by metric: Revenue: 3 consecutive misses; EPS (normalized): 2 consecutive beats.

Currency: USD · Scale: money in millions, absolute (per share) · Consensus is captured before each actual first became effective; analyst count shown per observation.

| Quarter | Metric | Consensus as of | Actual | Surprise | Outcome | Analysts |

|---|---|---|---|---|---|---|

| Q2 FY2026 | Revenue | 1,318 | 1,306 | -0.9% | Miss | — |

| Q2 FY2026 | EPS (normalized) | 1.97 | 2.07 | 5.3% | Beat | — |

| Q1 FY2026 | Revenue | 1,375 | 1,345 | -2.2% | Miss | — |

| Q1 FY2026 | EPS (normalized) | 1.82 | 1.85 | 1.6% | Beat | — |

| Q4 FY2025 | Revenue | 1,341 | 1,318 | -1.7% | Miss | — |

| Q4 FY2025 | EPS (normalized) | 1.67 | 1.62 | -3.0% | Miss | — |

| Q3 FY2025 | Revenue | 1,316 | 1,348 | 2.5% | Beat | — |

| Q3 FY2025 | EPS (normalized) | 1.53 | 2.16 | 40.7% | Beat | — |

| Q2 FY2025 | Revenue | 1,294 | 1,362 | 5.2% | Beat | — |

| Q2 FY2025 | EPS (normalized) | 1.38 | 2.01 | 45.7% | Beat | — |

| Q1 FY2025 | Revenue | 1,289 | 1,403 | 8.8% | Beat | — |

| Q1 FY2025 | EPS (normalized) | 1.37 | 1.61 | 17.5% | Beat | — |

| Q4 FY2024 | Revenue | 1,307 | 1,316 | 0.7% | Beat | — |

| Q4 FY2024 | EPS (normalized) | 1.48 | 1.46 | -1.4% | Miss | — |

| Q3 FY2024 | Revenue | 1,285 | 1,315 | 2.3% | Beat | — |

| Q3 FY2024 | EPS (normalized) | 1.52 | 1.74 | 14.7% | Beat | — |

Where the street disagrees

With no more than two estimates behind any line, dispersion signals are weak.

Currency: USD · Scale: money in millions, absolute (per share) · Dispersion is high-low divided by absolute mean; analyst count shown per item.

| Period | Metric | Mean | Low | High | Spread / mean | Analysts |

|---|---|---|---|---|---|---|

| Q3 FY2025 | Net income (GAAP) | 71.44 | 67.00 | 75.87 | 12.4% | 2 |

| Q1 FY2026 | Net income (GAAP) | 87.00 | 82.20 | 91.80 | 11.0% | 2 |

| Q3 FY2025 | EPS (GAAP) | 1.24 | 1.17 | 1.30 | 10.5% | 2 |

| Q1 FY2026 | EBITDA | 172.4 | 164.6 | 180.3 | 9.1% | 2 |

| Q3 FY2025 | EPS (normalized) | 1.53 | 1.47 | 1.60 | 8.5% | 2 |

Source: Visible Alpha consensus via S&P Xpressfeed · Consensus as of 2026-05-12 · generated 2026-07-19.

Model trust

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Coverage depth and vintage; broker count is the maximum represented.

| Brokers | Line items | Last revision |

|---|---|---|

| 1 | 154 | 2026-05-12 |

Caution: Coverage is thin at 1 broker.

Operating KPIs

The model carries no company-specific operating drivers, so only standardized financials are available.

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · FY-1A / FY0E / FY+1E; broker count shown per KPI.

| Operating KPI | Source | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|---|

| (Increase)/decrease in property, plant & equipment | SD | -73,686.00bn Amount | — | -88,000.00bn Amount | 1 |

| (Increase)/decrease in working capital | SD | 51,800.02bn Amount | 53,974.01bn Amount | -12,002.55bn Amount | 1 |

| Accounts payable | SD | 304,783.63bn Amount | 319,433.41bn Amount | 321,244.90bn Amount | 1 |

| Accounts payable and accrued expense | SD | 548,610.53bn Amount | 569,424.77bn Amount | 572,653.95bn Amount | 1 |

| Accounts payable, Average | SD | 304,052.31bn Amount | 312,108.52bn Amount | 316,367.54bn Amount | 1 |

| Accrued expense | SD | 243,826.90bn Amount | 249,991.36bn Amount | 251,409.05bn Amount | 1 |

| Assets / Equity(%) | SD | 237.0% | 208.2% | 188.6% | 1 |

| Assets turnover(x) | SD | 1.28 Ratio | 1.25 Ratio | 1.27 Ratio | 1 |

| Capital employed | SD | 3,132,791.12bn Amount | 3,308,932.32bn Amount | 3,366,158.05bn Amount | 1 |

| Capital employed, Average | SD | 3,076,388.06bn Amount | 3,220,861.72bn Amount | 3,287,139.88bn Amount | 1 |

| Cash & cash equivalents | SD | 403,432.31bn Amount | 617,808.53bn Amount | 597,790.81bn Amount | 1 |

| Cash & cash equivalents, Beginning | SD | — | 825,676.60bn Amount | 894,449.54bn Amount | 1 |

P&L bridge

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Margins are derived against revenue; YoY compares adjacent fiscal columns; broker count shown per line.

| P&L line | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|

| Revenue | 5,467,454.89bn Amount | 5,651,996.23bn Amount (3.4% YoY) | 5,844,021.84bn Amount (3.4% YoY) | 1 |

| Gross Profit | 1,327,206.38bn Amount (24.3% margin) | 1,347,761.00bn Amount (23.8% margin; 1.5% YoY) | 1,356,809.75bn Amount (23.2% margin; 0.7% YoY) | 1 |

| Ebitda | 713,441.81bn Amount (13.0% margin) | 735,176.72bn Amount (13.0% margin; 3.0% YoY) | 717,261.18bn Amount (12.3% margin; -2.4% YoY) | 1 |

| Operating Income | 541,955.81bn Amount (9.9% margin) | 603,776.72bn Amount (10.7% margin; 11.4% YoY) | 576,861.18bn Amount (9.9% margin; -4.5% YoY) | 1 |

| Net Income | 432,447.96bn Amount (7.9% margin) | 448,864.89bn Amount (7.9% margin; 3.8% YoY) | 416,825.20bn Amount (7.1% margin; -7.1% YoY) | 1 |

| Eps | 7.45 Amount | 7.70 Amount (3.3% YoY) | 7.13 Amount (-7.4% YoY) | 1 |

Consensus dispersion

With a single contributing broker on every item, minimum, maximum and quartiles collapse onto the point estimate and standard deviation is zero, so there is no consensus dispersion to interpret. Any disagreement in the investment debate is simply not visible in this data.

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Top high-low spreads relative to absolute mean; requires at least 3 brokers.

| Line item | Period | Mean | Min | Q1 | Q3 | Max | Spread / mean | Brokers |

|---|---|---|---|---|---|---|---|---|

| No qualifying dispersion | — | — | — | — | — | — | — | — |

Quarterly path

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Next four supplied quarters; final column is maximum broker coverage in the row.

| Quarter | (Increase)/decrease in property, plant & equipment | (Increase)/decrease in working capital | Accounts payable | Accounts payable and accrued expense | Accounts payable, Average | Total revenue | EPS Diluted, Applicable to common stockholders($) | Broker coverage |

|---|---|---|---|---|---|---|---|---|

| 4QFY-2026 | — | 68,269.57bn Amount | 319,433.41bn Amount | 569,424.77bn Amount | 306,497.65bn Amount | 1,388,840.90bn Amount | 1.98 Amount | 1 |

| 1QFY-2027 | — | -141,044.61bn Amount | — | — | 317,665.26bn Amount | — | 1.90 Amount | 1 |

| 2QFY-2027 | -22,000.00bn Amount | 41,125.33bn Amount | 307,483.04bn Amount | 527,113.78bn Amount | 315,661.70bn Amount | 1,464,204.93bn Amount | 1.79 Amount | 1 |

| 3QFY-2027 | -22,000.00bn Amount | 7,656.63bn Amount | 302,610.64bn Amount | 518,761.09bn Amount | 305,046.84bn Amount | 1,441,003.03bn Amount | 1.76 Amount | 1 |

181 stale period values omitted; 11 line items fully removed.

Source: S&P Capital IQ transcripts via Xpressfeed · latest indexed call 2026-05-07 · generated 2026-07-19.

Latest call digest

Maximus, Inc., Q2 2026 Earnings Call, May 07, 2026 · 2026-05-07T13:00:00

Q2 FY2026 call — May 7, 2026. Revenue of $1.31 billion landed in line with plan, with adjusted EBITDA margin of 14.4% and adjusted EPS of $2.07. Two unusual items — a $6.9 million ($0.09) software-asset impairment in U.S. Services and a $4.2 million (~$0.08) discrete R&D tax benefit — effectively offset in adjusted EPS. Management raised the FY2026 adjusted EPS guide for the second consecutive quarter to $8.25–$8.55 (up $0.20), lifted the full-year EBITDA margin guide to ~14.2%, and reiterated revenue of $5.2–$5.35 billion and free cash flow of $450–$500 million. It also raised its near-term EBITDA margin target range to 12%–15% and refreshed a $400 million buyback (≈$111 million repurchased in the quarter, $40 million more after quarter-end). Prepared remarks leaned on technology/AI-driven federal margin gains, fraud/program-integrity positioning, and building HR-1 (Medicaid work-requirement/SNAP) state opportunities, with one arrangement estimated to lift current program revenue by more than 30% and U.S. Services expected to return to mid-single-digit organic growth by Q4.

The Q&A was thin — a single analyst (CJS Securities) — and pressed the softer spots the prepared remarks skated over: an elevated 78-day DSO driven by administrative delays at one major federal customer and its effect on buyback capacity; why federal tech-efficiency gains have not yet reached the U.S. Services margin; the drivers of first-half state revenue declines against the promised Q4 recovery; and the still-undefined VA veterans-exam recompete timeline (contract runs to December 31, 2026, with an Industry Day pending).

Participant coverage from the latest call.

| Group | Participants | Count |

|---|---|---|

| Management | Operator; James Francis — Vice President of Investor Relations, Maximus, Inc.; David Mutryn — CFO & Treasurer, Maximus, Inc.; Bruce L. Caswell — President, CEO & Director, Maximus, Inc. | 4 |

| Analysts | Will Gildea — Equity Research Associate, CJS Securities, Inc. | 1 |

Curated latest-call exchanges; one row per analyst topic.

| Analyst | Firm | Topic | What changed in Q&A |

|---|---|---|---|

| Will Gildea | CJS Securities, Inc. | Elevated DSO and buyback capacity | Pressed on the higher DSO and repurchase capacity given cash lumpiness; management attributed it to one major federal customer with complex, retroactive invoicing and expects collections to catch up in Q4. |

| Will Gildea | CJS Securities, Inc. | HR-1 / SNAP offerings | Asked whether other SNAP solutions are being brought to market; management centered on the Accuracy Assistant tool plus wrapped BPO services and the Medicaid community-engagement (work-requirement) tool. |

| Will Gildea | CJS Securities, Inc. | State revenue decline vs. Q4 recovery | Asked what drove first-half U.S. Services declines and the basis for Q4 growth confidence; management cited prior-year clinical volumes and state-specific dynamics, with HR-1 activity underpinning the Q4 turn. |

| Will Gildea | CJS Securities, Inc. | Federal vs. Services margin gap | Asked why efficiency gains lifting U.S. Federal have not yet reached U.S. Services; management cited larger federal contract scale, state caution on AI adoption, patchwork state regulation, and legacy-system integration. |

| Will Gildea | CJS Securities, Inc. | VA recompete | Asked about VA contract timing, a possible extension, and an upcoming Industry Day; management said no formal rebid timeline has been released and the current contract runs through December 31, 2026. |

| Will Gildea | CJS Securities, Inc. | Remaining federal tough comps | Asked about further tough federal comparables in the back half; management flagged the prior-year fiscal Q3 clinical-volume surge as a continued tough comp. |

Theme tracker

Themes are curator-classified across supplied calls.

| Theme | Status | Quarters mentioned | Read-through |

|---|---|---|---|

| HR-1 / Medicaid work requirements & SNAP state opportunity | emerged | Q3 2025, Q4 2025, Q1 2026, Q2 2026 | Surfaced as the "Big Beautiful Bill" in August 2025 and has become the central state-side growth catalyst; management frames FY2026 as a shaping year with revenue contribution expected in FY2027 as final regulations solidify. |

| AI and automation as a margin lever | persisted | Q1 2025, Q3 2025, Q4 2025, Q1 2026, Q2 2026 | A recurring and increasingly emphasized driver of U.S. Federal margin expansion; management ties it to decoupling labor from volume and, in Q2 2026, raised the near-term margin target on this basis. |

| VA / veterans-exam recompete (PACT Act, MDE volumes) | persisted | Q4 2023, Q1 2024, Q2 2024, Q3 2024, Q1 2025, Q3 2025, Q1 2026, Q2 2026 | The most consistently pressed topic; the current contract runs to December 31, 2026 and the recompete timeline remains undefined, leaving a large federal program as an open question. |

| Medicaid redeterminations / unwinding tailwind | dropped | Q3 2023, Q4 2023, Q1 2024, Q2 2024, Q3 2024, Q1 2025 | The dominant FY2024 U.S. Services tailwind; management says the effort was complete by FY2025, and it is now absent as a driver and instead a year-over-year comp headwind. |

| Capital deployment — buybacks and disciplined M&A | persisted | Q4 2024, Q4 2025, Q1 2026, Q2 2026 | Repurchases stepped up as management calls the shares undervalued, alongside a stated bias toward federal defense / national-security acquisitions, all within a 2x–3x leverage target. |

Guidance ledger

Quotes, calls, and speakers are source-verified; outcomes are curator-classified.

| Verbatim guidance | Call | Speaker | Curator outcome | Outcome note |

|---|---|---|---|---|

| “adjusted EPS is projected to be between $5.70 and $6 per share” | Maximus, Inc., 2024 Earnings Call, Nov 21, 2024 · 2024-11-21T14:00:00 | David Mutryn | kept | Initial FY2025 range; raised repeatedly through the year and delivered adjusted EPS of $7.36 for fiscal 2025. |

| “We believe a reasonable range in the near term is 10% to 13% adjusted EBITDA margin.” | Maximus, Inc., 2024 Earnings Call, Nov 21, 2024 · 2024-11-21T14:00:00 | David Mutryn | kept | FY2025 came in at a 12.9% adjusted EBITDA margin, within the range; the target was later raised to 12%–15% in May 2026. |

| “adjusted EPS is projected to be between $7.95 and $8.25 per share” | Maximus, Inc., Q4 2025 Earnings Call, Nov 20, 2025 · 2025-11-20T14:00:00 | David Mutryn | pending | Initial FY2026 guide; subsequently raised to $8.05–$8.35 in February and $8.25–$8.55 in May, with the fiscal year not yet complete. |

| “Free cash flow for fiscal year 2026 is projected to be between $450 million and $500 million.” | Maximus, Inc., Q4 2025 Earnings Call, Nov 20, 2025 · 2025-11-20T14:00:00 | David Mutryn | pending | Reiterated on both the Q1 and Q2 FY2026 calls; delivery hinges on DSO normalizing below 70 days by year-end. |

| “Our adjusted EPS guidance increases by $0.10 and is now expected to range between $8.05 and $8.35 per share.” | Maximus, Inc., Q1 2026 Earnings Call, Feb 05, 2026 · 2026-02-05T14:00:00 | David Mutryn | pending | First FY2026 raise; increased again to $8.25–$8.55 in May 2026. |

| “Our adjusted EPS guidance increases by $0.20 and is now expected to range between $8.25 and $8.55 per share.” | Maximus, Inc., Q2 2026 Earnings Call, May 07, 2026 · 2026-05-07T13:00:00 | David Mutryn | pending | Second consecutive raise; fiscal year ends September 30, 2026. |

Q&A pressure map

Question counts and firms are curator tallies; analyst coverage shown above.

| Topic | Questions | Firms | Pressure / response |

|---|---|---|---|

| VA / veterans-exam contract and recompete | 15 | CJS Securities, Inc., Raymond James & Associates, Inc., Research Division, Stifel, Nicolaus & Company, Incorporated, Research Division | Pressed in nearly every call across all three brokers, most recently on rebid timing and a possible extension; management has consistently declined to give a firm recompete timeline. |

| Margin durability and technology-driven efficiency | 12 | CJS Securities, Inc., Raymond James & Associates, Inc., Research Division, Stifel, Nicolaus & Company, Incorporated, Research Division | Recurring probing on how sustainable the margin gains are and why they show up in Federal but not yet in U.S. Services. |

| Medicaid redeterminations / unwinding | 9 | Stifel, Nicolaus & Company, Incorporated, Research Division, Raymond James & Associates, Inc., Research Division, CJS Securities, Inc. | Heavily pressed through FY2024 as analysts sized the tailwind and its wind-down; faded as the exercise completed. |

| HR-1 / Big Beautiful Bill / SNAP opportunity sizing | 5 | CJS Securities, Inc., Raymond James & Associates, Inc., Research Division | Repeated attempts to quantify the state opportunity; management has kept answers qualitative on scope and timing, pointing to FY2027 for revenue. |

| Cash flow, DSO and buyback capacity | 4 | CJS Securities, Inc., Raymond James & Associates, Inc., Research Division, Stifel, Nicolaus & Company, Incorporated, Research Division | Pressed on free-cash-flow rhythm and, more recently, elevated DSO and its constraint on repurchases; management ties the drag to one federal customer. |

Language shifts

Only language evidence verified against the referenced component is shown.

| Observation | Verbatim evidence | Call ID | Component |

|---|---|---|---|

| Management lifted its near-term margin ceiling, signaling greater confidence in the durability of technology-driven gains versus the 10%–13% target set the prior year. | “we are raising our near-term adjusted EBITDA margin target range to 12% to 15%” | 1994106528 | 2 |

| New procurement-risk vocabulary entered the prepared remarks, flagging slower federal awards and rising protests as a timing headwind. | “awards have shifted right, protests have increased, further delaying outcomes” | 1994106528 | 3 |

| Cash-collection caution became a repeated theme, with elevated DSO tied to a single federal customer rather than broad demand. | “ongoing administrative delays at a major federal customer” | 1994106528 | 2 |

The call history shows a management team that has repeatedly raised earnings guidance on technology-driven margin gains while the top line laps its own FY2024–FY2025 volume surges. For the current debate, the swing factors are the unresolved VA recompete and whether the HR-1 / SNAP state pipeline converts into the FY2027 revenue management keeps promising.

The company in one look

Maximus runs the administrative machinery behind government benefit programs. It answers the Medicare help line, verifies Medicaid eligibility for states, examines veterans' disability claims, and operates welfare-to-work programs — work that generated $5.43 billion of revenue in fiscal 2025 [1], essentially all of it from government customers [2]. The stock has fallen from roughly $99 in January 2026 to $58, and now trades at about 7 times guided earnings and a 12% free-cash-flow yield. This report tests whether that cash flow is durable.

Revenue FY2025 ($M)

Adj. EBITDA Margin

Free Cash Flow FY2025 ($M)

FCF Yield (trailing)

Sources: FY2025 Form 10-K — revenue [3], Adjusted EBITDA margin [4], free cash flow [5]; FCF yield derived on a $3.06B market capitalization (52.5M shares at $58.30).

What Maximus does

Maximus was founded in Virginia in 1975 and describes itself as a provider of tech-enabled services to government, touching more than 100 million American citizens plus programs in the U.K., Canada, and the Middle East [6]. Its role is narrow and specific: it translates public policy into operating models — call centers, eligibility systems, clinical assessment networks — that deliver a government program at scale, for a fee. It does not set policy or fund the benefits; it runs the delivery.

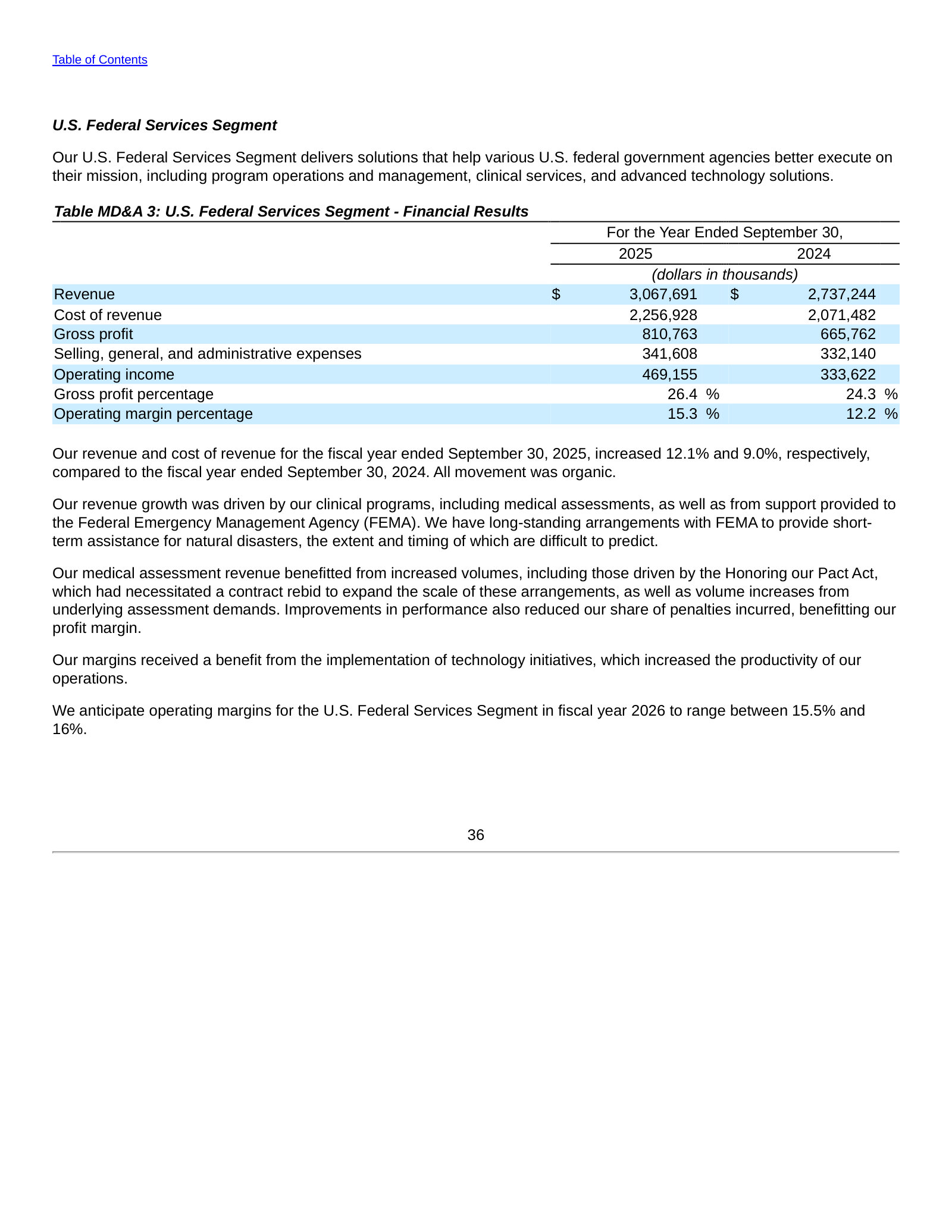

The business reports in three segments. U.S. Federal Services, the largest and most profitable, runs federal contact centers and clinical-assessment work, including the Veterans Evaluation Services network. U.S. Services administers state health-and-human-services programs — Medicaid enrollment, child support, employment services. Outside the U.S. is a smaller employment-and-health-services operation concentrated in the U.K.

Source: FY2025 Form 10-K, Note 3 Business Segments [7].

The concentration is the defining feature. In fiscal 2025, about 55% of revenue came from the U.S. federal government and about 33% from state and local agencies — roughly 88% from government, with most of the rest from national governments abroad [8]. It is concentrated further within that: roughly 60% of revenue came from the ten largest contracts, and about one-fifth from a single federal agency [9]. This is a company whose fortunes are tied to a small number of government relationships.

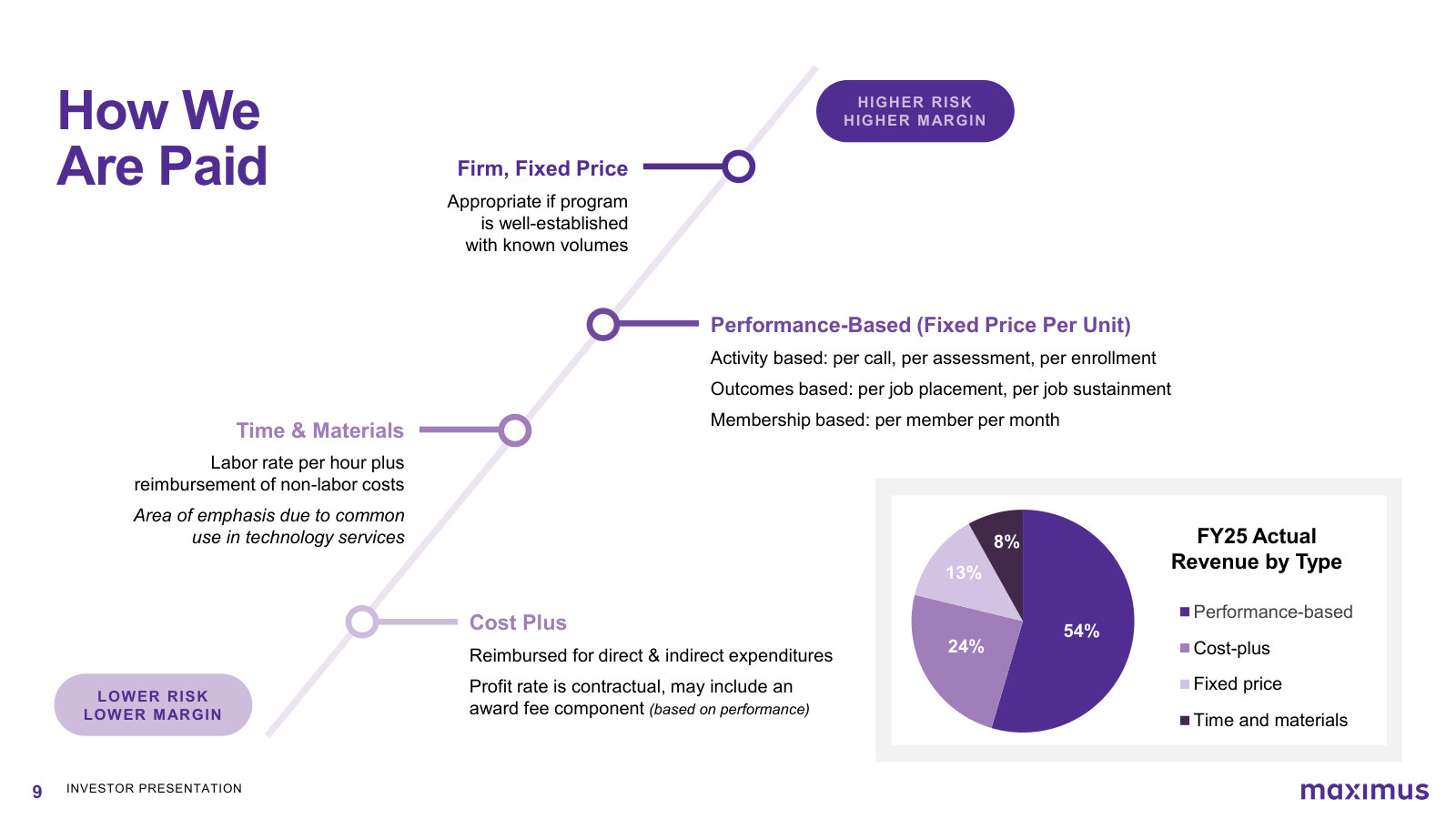

How it gets paid matters for the cash-flow question. About 54% of revenue is performance-based — paid per transaction or per outcome, such as a completed medical exam or a sustained job placement — and 13% is fixed-price; the balance is cost-plus and time-and-materials work [10]. Performance-based contracts carry estimation risk but tend to scale with citizen activity rather than headcount, which is central to the margin story developing now.

Scale and trajectory

Revenue has grown from about $2.45 billion in fiscal 2017 to $5.43 billion in fiscal 2025 — roughly a 10% annual rate over eight years, and a 9.4% five-year compound rate [11]. Two acquisitions in 2021 — the Veterans Evaluation Services and federal-technology businesses — roughly doubled the goodwill on the balance sheet and lifted federal exposure. Operating cash flow has been positive every year but lumpy, ranging from $245 million to $517 million over the period, a pattern the reader focused on cash-flow consistency will want to test.

Source: FY2025 Form 10-K, Consolidated Statements of Operations and Cash Flows; prior-year figures per company filings, as reported [12].

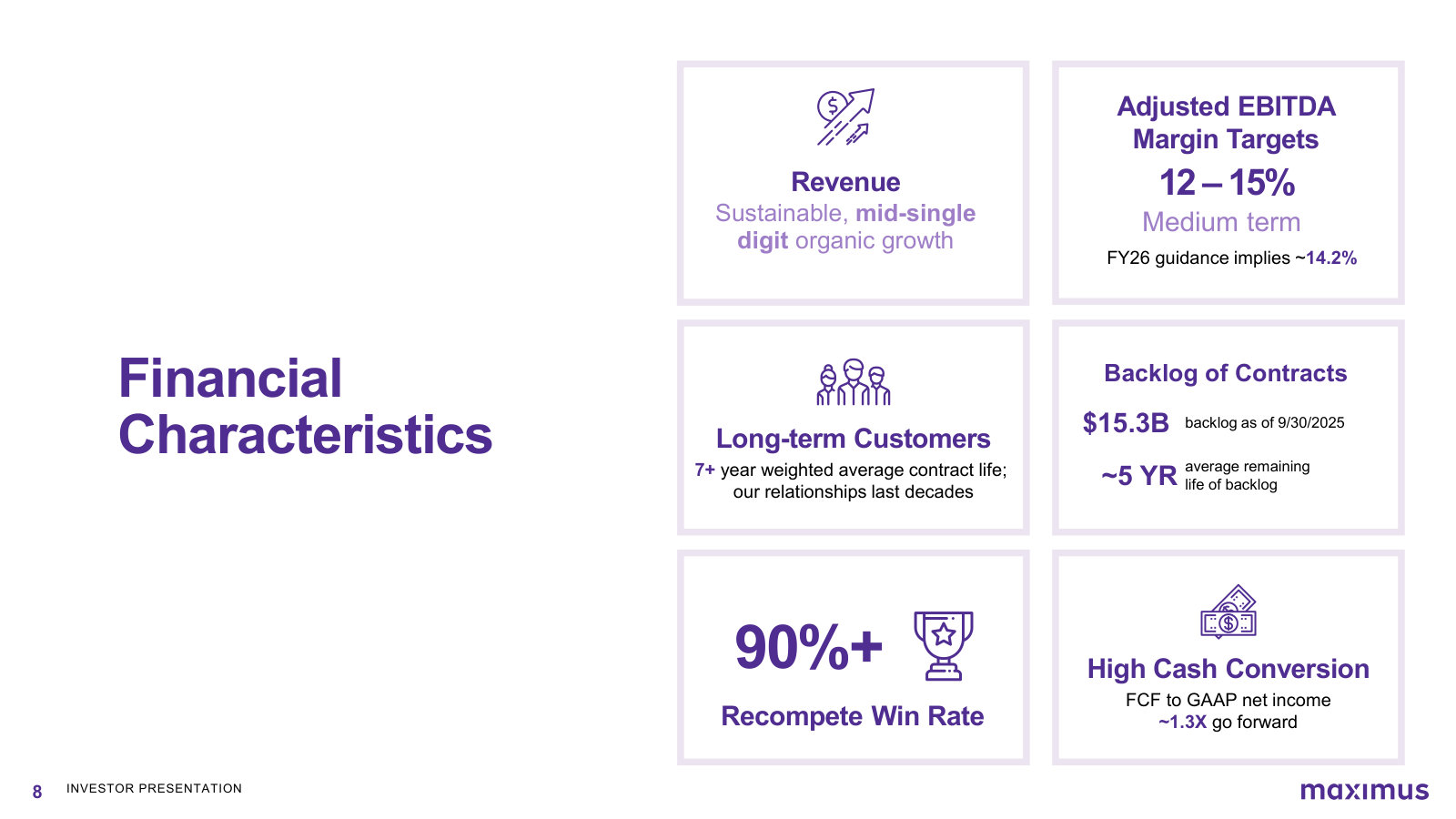

Contracted backlog stood at $15.3 billion at September 30, 2025 — about 2.8 times annual revenue — which gives the top line reasonable forward visibility, though the company cautions it may not realize all of it [13].

The economics

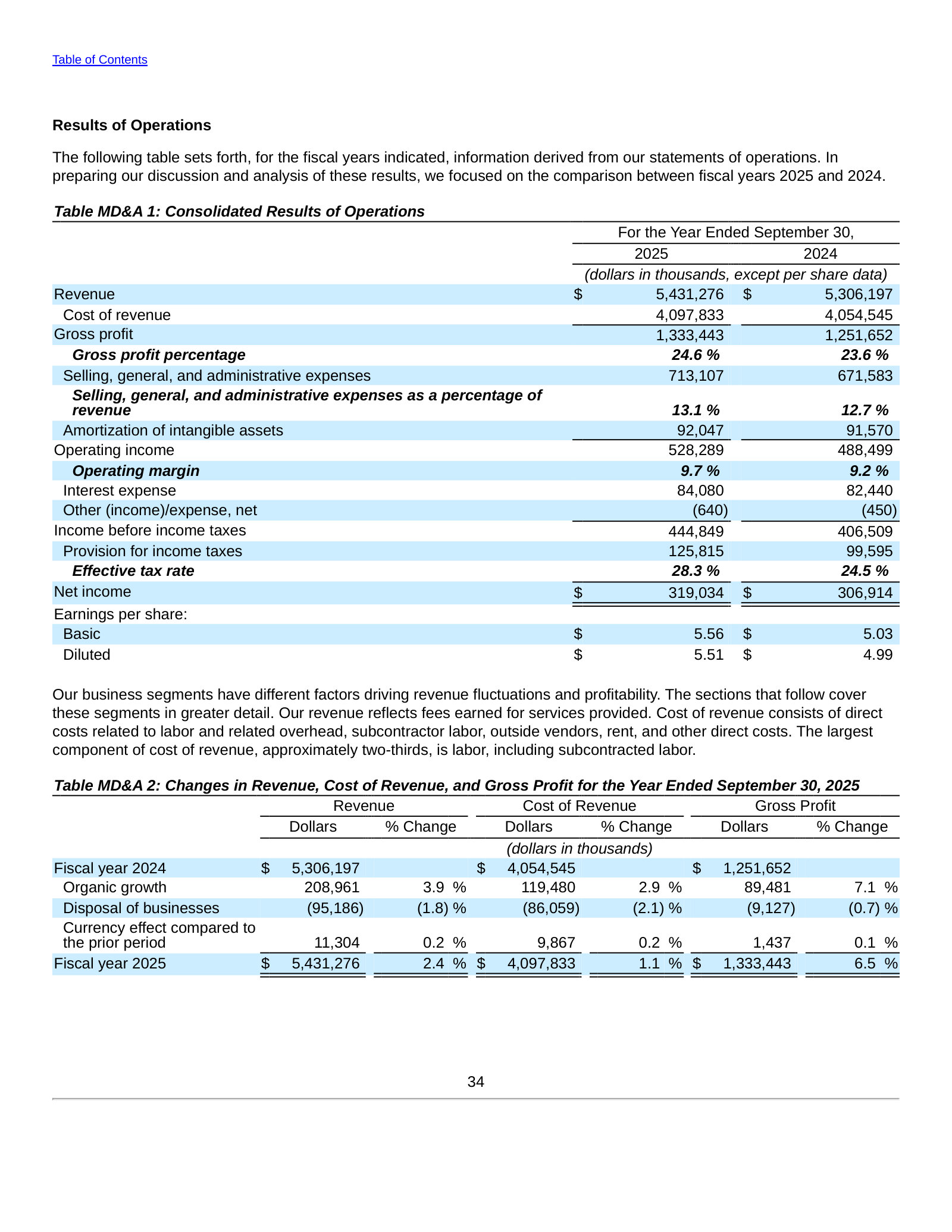

This is an asset-light services model. Capital expenditure was $63 million in fiscal 2025 against $429 million of operating cash flow, so free cash flow was $366 million; the prior year converted $515 million of operating cash flow into $401 million of free cash flow [14]. Operating margin was 9.7% [15] and Adjusted EBITDA margin 12.9%; on an adjusted basis that excludes acquisition intangible amortization, diluted earnings were $7.36 per share versus $5.51 reported [16].

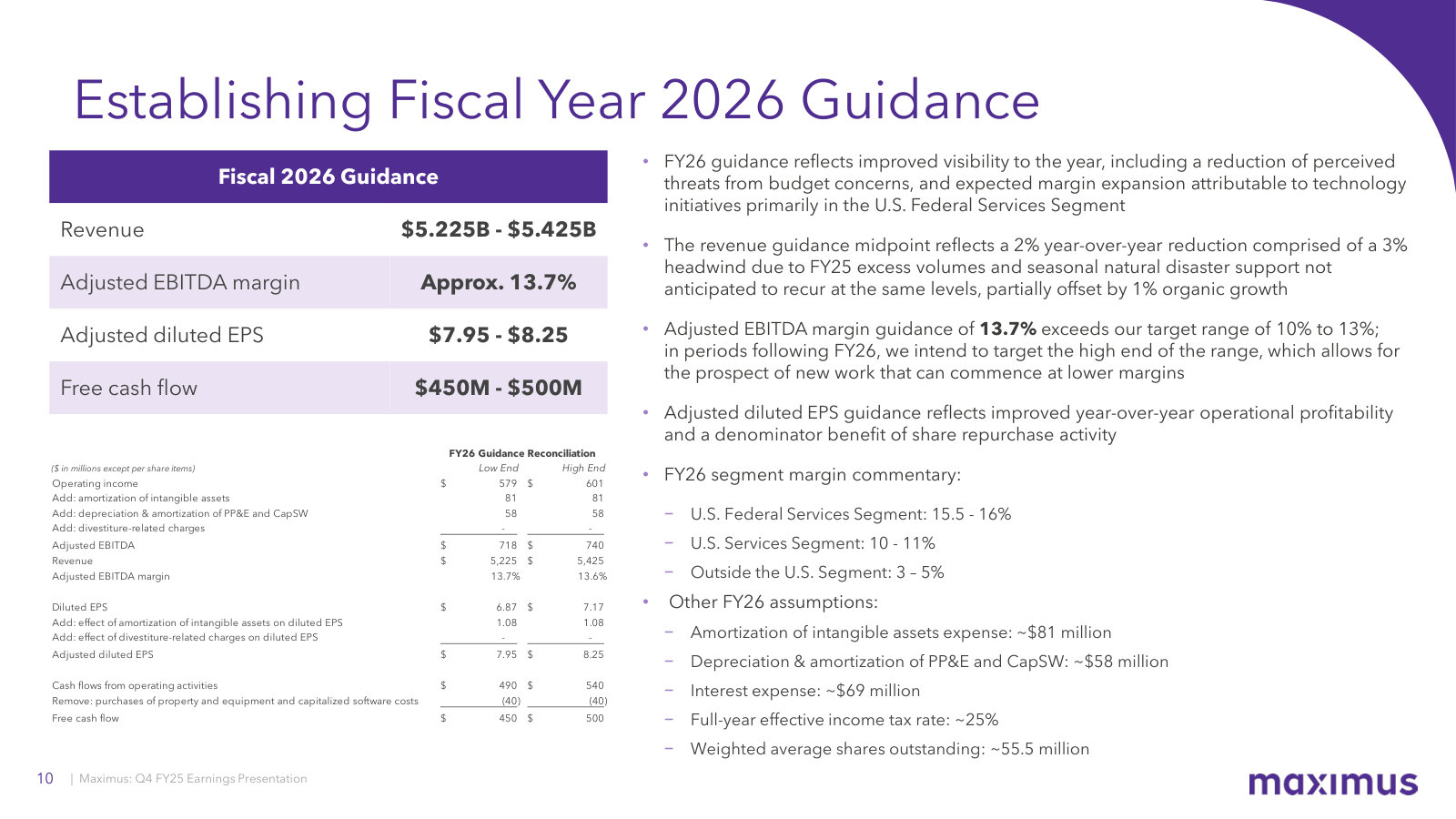

The recent operating story is margin, not growth. Management credits automation and AI tools that "decouple labor costs from our ability to process more volumes" — the same forces that let a per-transaction contract earn more without adding people [17] — and on that basis has guided the federal segment to a 17.5% full-year operating margin and raised its near-term Adjusted EBITDA margin target to 12–15% [18]. Against that, revenue is guided to be roughly flat-to-down in fiscal 2026 at $5.2–5.35 billion as elevated pandemic-era and natural-disaster volumes roll off; adjusted EPS is guided to $8.05–8.55, up about 14%, and free cash flow to $450–500 million [19]. Earnings and cash are being guided higher even as the top line pauses.

Balance sheet and capital return

Maximus carries net debt — about $1.4 billion at March 31, 2026 against $157 million of cash — but leverage is moderate at 1.75 times EBITDA on the credit-agreement definition, inside its own 2–3x target [20]. Because goodwill and intangibles (about $2.3 billion) exceed book equity ($1.7 billion), tangible book value is negative — normal for an acquisitive services business, but a reason tangible price-to-book is not a useful anchor here [21].

Capital return has stepped up sharply. In fiscal 2025 the company repurchased 5.8 million shares for $462 million [22], and it kept buying into the 2026 decline, authorizing a fresh $400 million program in May 2026 while stating it prioritizes repurchases "when we believe our share price does not reflect the intrinsic value of the business" [23]. Shares outstanding have fallen from 60.4 million in September 2024 to 52.5 million by May 2026, a 13% reduction, alongside a $1.20 dividend [24].

Sources: FY2025 Form 10-K, Statements of Changes in Shareholders Equity [25]; Q2 FY2026 Form 10-Q cover, 52,540,363 shares outstanding as of May 4, 2026 [26].

The stock and what the price implies

The share price roughly doubled from late 2023 to an all-time high near $99 in January 2026, then fell about 41% to $58 by July 2026 — the drop coinciding with fiscal-2026 guidance for flat-to-lower revenue and a working-capital build that pushed days-sales-outstanding to 78 days at a large federal customer [27], with the veterans-exam contract — the anchor of the 2021 acquisition — running through December 2026 and due for recompete [28]. An earlier, smaller drawdown in early 2025 followed the launch of the federal Department of Government Efficiency (DOGE), whose stated goal of cutting federal spending is a direct risk to a contractor that draws most of its revenue from Washington [29].

Source: market price data, as reported; period-end and 52-week-high closing prices.

What the reader gets at $58 is a specific arithmetic. On a $3.06 billion market capitalization, trailing free cash flow of $366 million is a 12.0% yield, and the $450–500 million guided for fiscal 2026 would be roughly 15%. Enterprise value of about $4.4 billion is 6.3 times fiscal-2025 Adjusted EBITDA, and the price is near 7 times the midpoint of guided adjusted EPS — with the share count still shrinking.

Source: derived from FY2025 Form 10-K figures [30] [31], FY2026 guidance [32], and market price; leverage per the Q2 FY2026 10-Q [33].

Multiples this low usually price a business the market believes is about to shrink. The bull case is that the fear is misplaced: much of Maximus's work runs mandatory programs — Medicare, Medicaid, veterans' benefits — that persist across administrations, and its state contracts are paid by citizen activity, so tighter eligibility rules can raise transaction volumes even as they cut the benefit rolls [34]. The bear case is equally concrete: 60% of revenue sits in ten contracts, one-fifth in a single agency, the largest of those faces recompete, and DOGE is an explicit effort to spend less on exactly this kind of vendor.

What this report tests

The reader's standard is a durable moat that keeps free cash flow strong — even if it stops growing — for at least a decade. Maximus arrives with the cash-flow economics that standard rewards: a 12% trailing free-cash-flow yield, 1.75x leverage, and a shrinking share count, all after a selloff that halved the equity while management guided cash flow higher. Durability is the open question, and it runs through every chapter that follows: